By Mohneet Dhir, multi-asset product specialist, Vanguard, Europe

There’s no sugar-coating the fact that 2022 has been painful for multi-asset investors and further volatility is possible as key economies flirt with recession.

Global bonds posted their worst first-half returns in decades this year amid rising inflation and interest-rate expectations, while global equities delivered negative double-digit returns. This left some investors questioning the long-term benefits of maintaining a core allocation to high-quality fixed income.

While the recent rebound in global bond prices (and fall in yields) should offer some comfort to clients, there are three further points that should provide some reassurance to investors unnerved by the economic environment.

1. High-quality bond returns tend to be uncorrelated with equity markets

It’s important to remember that the primary reason for investing in high-quality fixed income is to provide a buffer against equity market shocks, and not to drive returns. It’s entirely understandable that the simultaneous drop in global equity and bond markets this year has been difficult for investors to stomach. But it can and does happen – roughly 30% of the time over the past 20 years, according to Vanguard research.

Still, the longer equity markets decline, the more likely bonds are to play a stabilising role in a portfolio. While the dynamics affecting asset correlations are complex, a key driver is if economic growth and interest rates are moving in the same direction. When they do, the correlation between equities and bonds tends to be negative.

That’s because policy-rate changes are dictated by economic conditions: if equity markets crash, central banks tend to support their economies by cutting interest rates and pushing bond total returns higher. If, instead, inflation is rising because the economy is growing and the labour market is tight, rates are increased and bond returns become negative.

If rates are rising when the economy is cooling, as has been the case recently, bonds and equities tend to be more positively correlated. Also, the stock-bond correlation tends to turn positive when inflation is rising faster than expected.

Looking ahead, we believe the impact of future rate rises has now largely been priced in and that bonds will resume their role as an effective hedge against equity risk. Fears of weaker economic conditions are likely to only strengthen the risk-diversifying role of bonds.

2. Global hedged bonds have dampened risks in previous rate-rising cycles

The recent downturn in markets has been fuelled largely by rising headline inflation and interest rate expectations, with UK headline inflation hitting a 40-year high of 10.1% in July. The Bank of England, Federal Reserve and European Central Bank have all been increasing interest rates and look set to raise them further in their efforts to stifle inflation.

Historically a core allocation to global hedged bonds has served multi-asset investors well through most market environments, including a rapid rate-rise scenario.

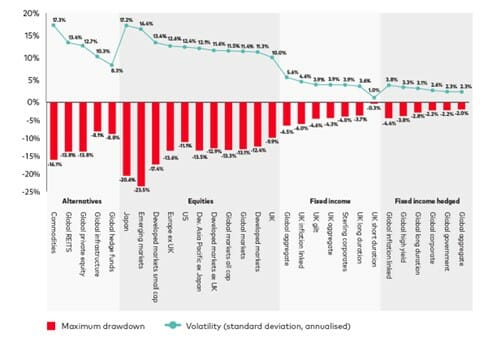

When US interest rates rose 425% between June 2004 and July 2005, hedged global bonds were among the best risk dampeners. As the chart below demonstrates, the asset class experienced low volatility and drawdowns relative to alternatives, equities, fixed income and their major sub-asset class categories as rates rose quickly.

Maximum drawdown and volatility amid 425% rise in US rates

Past performance is not a reliable indicator for future results

Source: Vanguard calculations based on data from Bloomberg. Notes: Data is for the period from 1 June 2004 to 31 July 2006 (extracted from analysis between 1 June 2004 and 22 May 2022). Returns calculated in GBP. Annualisation is based on weekly total returns5.

When we analysed the maximum drawdown and volatility of the same assets over a longer time frame – from June 2004 to May 2022 – global hedged bonds again proved to be one of the best risk dampeners. That’s an 18-year period that also covers the global financial crisis, the modest rate rises between 2015 and 2019, and the Covid-19 crisis in 2020.

3. Return outlook for bond and multi-asset investors has improved

The current silver lining for long-term investors is that the worst is probably behind us. The fall in bond prices seen to date means yields have adjusted higher. While there may well be more repricing to come in the next year or so, it means the return outlook for bond investors is better now than at the beginning of the year.

Our latest 10-year return forecasts suggest UK-based investors can expect an annualised return from domestic bonds of around 4.6% to 5.6% over the next decade and one of between 4.2% and 5.2% from global hedged bonds (ex-UK). That’s up from 0.8% to 1.8% for both local and domestic bonds at the beginning of the year. It’s a similar picture for multi-asset investors. Our 10-year nominal return expectations for traditional equity/bond portfolios are up since the beginning of the year

Keeping an eye on long-term value

Market trends can and do change. There’s no way of predicting market movements over the short term, but we think the data makes a strong case for maintaining a broadly diversified exposure to high-quality fixed income as part of a balanced portfolio of equities and bonds.