The COP is designed to help solve one of the world’s most urgent problems: climate change.

Last year’s event in Glasgow was all about planning (or planning to make plans), while the nitty gritty of implementation was largely deferred to this year’s event, COP27, in Egypt.

Investors are increasingly engaged in climate-related issues and are likely to follow COP27 with interest. We talk to David Kneale (pictured), Head of UK Equities at Mirabaud Asset Management, about what COP means for investors, how companies are responding to climate change pressures and how much real progress has been made in the race to zero.

Q: Did any of the COP26 pledges filter down to have a material impact on the companies in your investment universe?

A: The biggest impact of COP26 has probably been felt in the financial services sector. The Glasgow Financial Alliance for Net Zero has reinforced and co-ordinated the work of groups such as the Net Zero Asset Managers initiative (NZAM), to which Mirabaud Asset Management is a signatory.

NZAM has drawn together 292 asset managers, with a collective AuM of USD68 trillion (as at 27 October 2022), which are committed to achieving net zero alignment by 2050. However, this won’t be possible without detailed disclosures and action plans from the companies owned within these asset managers’ funds, hence the drive for comprehensive disclosures and emissions reduction target setting has continued to gather pace.

There is something of a lag before materials are produced by companies, but during this round of sustainability reporting, we would expect all of our portfolio companies to be providing greenhouse gas (GHG) emissions data and well over half to have established emissions-reduction targets: a pattern we expect to see repeated across the UK equity market more broadly.

Q: Are COP27 outcomes of critical importance to investors, or are companies influenced by other pressures when it comes to climate change?

The ‘measuring’ and ‘promising’ elements associated with climate change have built up an unstoppable level of momentum. Not reporting GHG emissions is rather like not reporting revenue…unacceptable for a listed company. But the crunch point is delivering on the promises, which is where high-profile events like COP can help to encourage action.

I fear delivery has been materially impacted by recent events. Many businesses have been in crisis management mode for three years as a result of pandemic protocols, supply chain bottlenecks, the war in Ukraine, the energy crisis, spiking inflation and imminent recession. Companies, especially smaller ones, need a period of stability to free up management and financial resource to meaningfully address these challenges.

Investors have been forgiving of this, but if underlying portfolio companies begin to prevent asset managers from meeting their own NZAM commitments, these conversations could become tense.

Q: Which COP27 topic do you think could most impact equity investors?

I think the elephant in the room at this year’s event is going to be ‘loss and damage’.

The standout image from COP26 was Tuvalu’s foreign minister presenting knee-deep in the Pacific Ocean to highlight rising sea levels and coastal erosion. Countries such as Tuvalu did nothing to create these catastrophic environmental problems yet are going to incur costs they cannot possibly bear.

The finger of blame is pointing firmly at high-emitting countries.

The Glasgow Dialogue, intended to address these issues, has delivered little. Why? The potential sums of money involved with ‘loss and damage’ financing are mind-boggling, which explains why no-one is keen to act, but movement here could have momentous implications for investors.

Q: Adaption to inevitable environmental changes is a concept you’ve highlighted previously as an investment challenge. Are the companies you look at factoring this in?

This is such a good question. The answer for companies generally is ‘not really’. However, a key part of our investment process leads us away from those businesses that risk being most badly impacted.

Today, the probability of damaging environmental events is rising, but day-to-day everything is essentially normal. The changes required to address this deterioration are very significant: relocating large, expensive fixed assets; reconfiguring supply chains; finding entirely new customer bases. As such, what we’ve seen to-date is enormous inertia.

One of the positive effects of improved disclosures, as well as the introduction of policies on water consumption, waste reduction etc, combined with the expectation of board-level responsibility for these matters, has been to bring many of these issues to the surface.

We have seen a growing number of our portfolio companies factoring future water availability into capital allocation decisions and building additional flexibility into supply chains. The best in class are going a step further and working directly with their existing supply chains to improve resilience.

Q: What climate-related disclosure trends have you seen UK companies adopting?

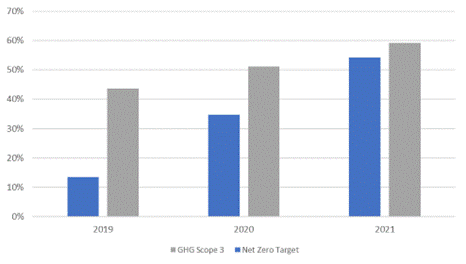

Looking across the FTSE All-Share and AIM 100 indices, 60% of companies now disclose Scope 3 GHG emissions. This rises to more than 75% of companies with >GBP1 billion market cap. More than 50% of companies have committed to net zero targets, rising to 70% for companies >GBP1 billion market cap. This figure is materially lower for the science-based targets, but as a newer metric, it is likely to catch up quickly.

Chart 1: UK companies are committing to change

Q: So, we have a good idea of what’s being emitted and what’s being committed, but are we seeing much improvement?

This is a surprisingly complicated question to answer. As commodity prices have been enormously volatile, the biggest emitters in the UK − oil and mining companies − have seen huge variations in revenue per tCO2e. Does this count as improved efficiency or just noise?

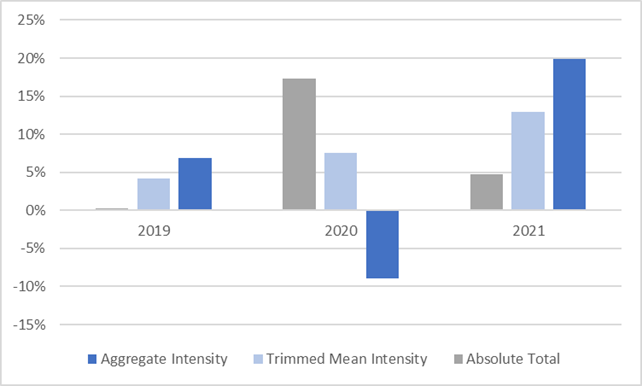

Chart 2 covers all the bases: the improvement of total CO2 emissions (grey – boosted dramatically by everyone being locked up in 2020 due to Covid), the improvement in aggregate intensity (dark blue – total CO2 vs total sales declined in 2020 as commodity prices collapsed, meaning the biggest emitters generated dramatically less revenue) and the more stable, and arguably most meaningful, improvement in trimmed mean intensity (light blue – the reduction in CO2 emissions vs revenue for the non-weighted average UK business).

Over the three years, the overall story is consistent: total emissions down 21%, aggregate emissions intensity improved 19% and trimmed mean emissions intensity improved 26%.

Chart 2: Emissions summary – 2019-2021

Before celebrating too wildly, 2022 is going to be a very interesting data point: activity levels will have normalised after Covid, with increased travel across all industries. Strains on energy supplies will become apparent, as will the extent to which most commodity industries have been ramping up production.

My expectation is that the trimmed mean will hold its improvements in efficiency. Unfortunately, the bulk of this gain is due to the reduction in emissions from the UK’s shifting electricity generation mix (more renewable generation has reduced CO2 per kWh by ~15% over the last three years), rather than corporate endeavours. If we allow for some inflation in selling prices over this period, then there will have been little material change in emissions efficiency from the individual actions of most businesses.

They have measured, they have promised (their owners have relied on their promises to make more promises), next comes the tricky part…

David Kneale, Head of UK Equities within Mirabaud Asset Management, has experience in the portfolio management industry since 1999. Prior to joining Mirabaud Asset Management in November 2001, David spent four years in charge of a management consultancy team covering life insurance and asset management companies. David previously worked at Arkwright as Senior Associate and Strategy Consultant and also at Halogen, a management consulting group, where he ran a team of eight consultants, undertaking projects for multinational investment management organisations. David Kneale graduated from Worcester College Oxford, where he read Geography, and holds the Investment Management Certificate.