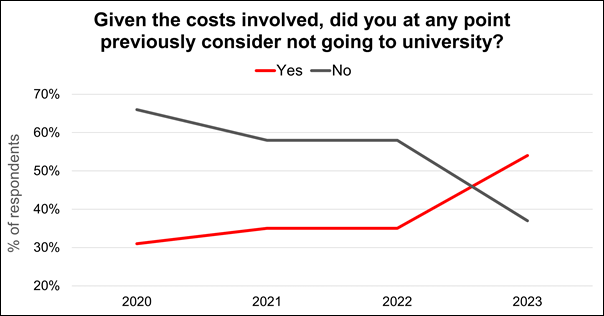

With A-Level results day approaching on 17 August, many anxious school leavers will be considering what comes next. More than half of current or prospective university students (54%) have considered not going to university because of the costs involved, according to the results of an annual survey1 from the Association of Investment Companies (AIC).

This is the highest percentage since the question was first included in the survey in 2014. In 2020, 2021 and 2022, the comparable percentages were 31%, 35% and 35% respectively.

Source: AIC/Opinium Research

In a further sign of financial strain, less than three-fifths of students (59%) believe it is realistic for their parents to help them financially while they are at university, down from almost two-thirds (65%) last year. Not surprisingly, ability to help is related to social class, with 65% of students from families from social grades ABC1 believing their parents will help versus 47% of students from social grades C2DE.

Covid’s long shadow

Like the virus itself, the impact of Covid-19 on students’ experience and expectations of university is still lingering. Around four-fifths (81%) of graduates who were at university when the pandemic started say that it made their time at university worse value for money. Among current students, a majority (57%) say that Covid-19 has made their time at university worse value for money.

Around a quarter (24%) of students say they considered not going to university at some point because of Covid.

Will students ever pay off their debt?

With the government announcing plans this year to extend the period after which student loans are written off from 30 to 40 years, more students think they will eventually pay off their debt than in last year’s survey – but it’s still a minority.

Over two-fifths (44%) of students who have a student loan, or who are planning to have one, believe they will eventually pay it off in its entirety, compared to 32% in last year’s survey.

However, there is a marked difference between male and female students, with 60% of male students believing they will eventually repay their whole loan versus 33% of their female peers.

Parents do what they can to help

Among parents with children at university, or who expect their children to go, supporting their children through their degrees is still a clear priority. Over half of parents surveyed (52%) consider this to be the highest priority when it comes to helping their children out financially, with 31% of respondents prioritising contributing to a first house purchase, 7% a car, and 5% travel.

However, more than three-quarters of parents (76%) say the rising cost of living has made it more difficult to help.

Parents overwhelmingly favour cash savings when it comes to ways to save for their children. Nearly two-thirds (63%) of respondents use cash, with only 16% using shares, 15% investment trusts, 11% bonds and 10% property (respondents could select more than one option). Over four-fifths (85%) of parents have saved or invested for their children’s future.

Only about a fifth (19%) of parents realise that it’s possible to invest in the stock market for as little as £25 a month, with 41% believing minimum investments were higher than that and a further 41% not sure.

Annabel Brodie-Smith, Communications Director at the Association of Investment Companies (AIC), said: “The cost of university is clearly putting increasing pressure on both students and parents. While it’s encouraging to see the overwhelming majority of parents saving for their children’s future, it’s clear that only a minority are taking advantage of the long-term growth potential the stock market has to offer.

“Investment companies can offer diversified access to the stock market and are suitable for investors who are putting money away for periods of at least five years, but preferably ten or longer. They can make great investments for parents who are saving for children. However, any stock market investment can go down as well as up. If parents aren’t sure whether investing in the stock market is right for them, they should consult a qualified financial adviser.”