The Chancellor Jeremy Hunt has reduced the main rate of National Insurance for employees by 2p in his Autumn Statement and overhauled NI for the self-employed.

Currently, employees pay 12% Class 1 National Insurance on earnings over £12,570, and 2% on earnings over £50,270. The cut means that from 6 January 2024 employees will pay 10% and 2% respectively.

For the self-employed, from 6 April 2024 the flat-rate of Class 2 NIC will be abolished and the Class 4 rate will be cut from the current 9% to 8% on profits between £12,570 and £50,270. The rate remains at 2% on profits over £50,270.

These moves will affect about 29 million people in the UK who earn an income from work.

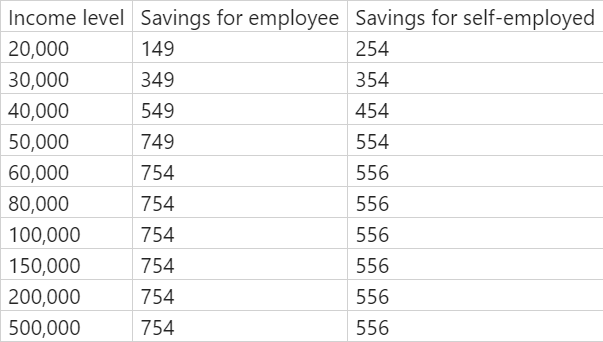

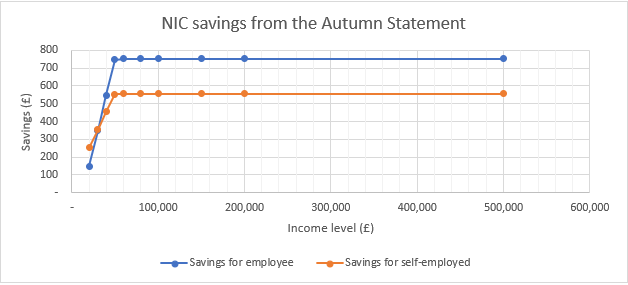

The tax team at professional services and wealth management firm Evelyn Partners have crunched the numbers for the impact at various income levels for the employed and the self-employed.

Evelyn Partners’ Head of Tax Sian Steele, says:

“A bit more take-home pay will be very welcome to millions of workers and the Chancellor was keen to present a fresh narrative of tax cuts. Despite Mr Hunt’s emphasis on the self-employed, our table shows that the gain in take-home pay across many income levels is greater for the employee.

“But these reductions in NI – costing the Treasury £9billion of the £172billion total take from this tax – will do little to counteract the rising tide of direct taxation that has taken the overall tax burden to the highest levels in 70 years. [1]

“To put it into perspective, the freeze policy on tax thresholds* that has been in place since 2021 – as well as the cut to the additional rate threshold to £125,140 in April 2023 – will be earning £29.3 billion a year for the Treasury by 2027-28. That is equivalent to a 4p increase in the basic rate of income tax. [2]

“That substantial shift in the tax landscape is driven largely by the fiscal drag effect as the incomes of millions of people surge across the personal allowance and the higher and additional rate thresholds – so that people start to pay tax for the first time, or are drawn into paying tax at higher marginal rates.

“Hunt has favoured NI over an income tax cut for various probable reasons. NI is focused specifically on income from work, while income tax applies to a number of other sources of income, so an NI cut can be presented as an incentive and a reward to workers, while also having the benefit of being cheaper for the Treasury.

“You do not pay NI on any private pension income or at all after state pension age**, so that most retirees will not benefit from this cut – and so it can perhaps deflect some criticism from any perceived inter-generational “unfairness” of hiking the state pension by a hefty amount under the triple lock.”

*Excepting the NI threshold rise in 2022/23 that brought the starting level band in line with the annual personal income tax allowance at £12,570.

**Class 4 NICs can continue until the end of the tax year when a worker reaches state pension age.

![[UNS] tax](https://ifamagazine.com/wp-content/uploads/2024/11/getty-images-gA9N92x8Yko-unsplash.webp)