In this analysis, Chris Ainscough, Director of Asset Management, Charles Stanley, walks us through the four main levers for fixed income investing and why he believes that an active and targeted asset allocation strategy is so important.

The volatility in fixed income markets over the past two years has taken many investors by surprise. The risk and reward profile for a range of fixed income assets has been subject to significant change, wrong-footing those with a static fixed income allocation. To capture opportunities and manage risks, active management of an investor’s fixed income allocation is crucial.

There are four main levers for fixed income investment. The first is duration, which governs a bond’s sensitivity to interest rates. It is calculated with reference to a bond’s yield, coupon and call features.

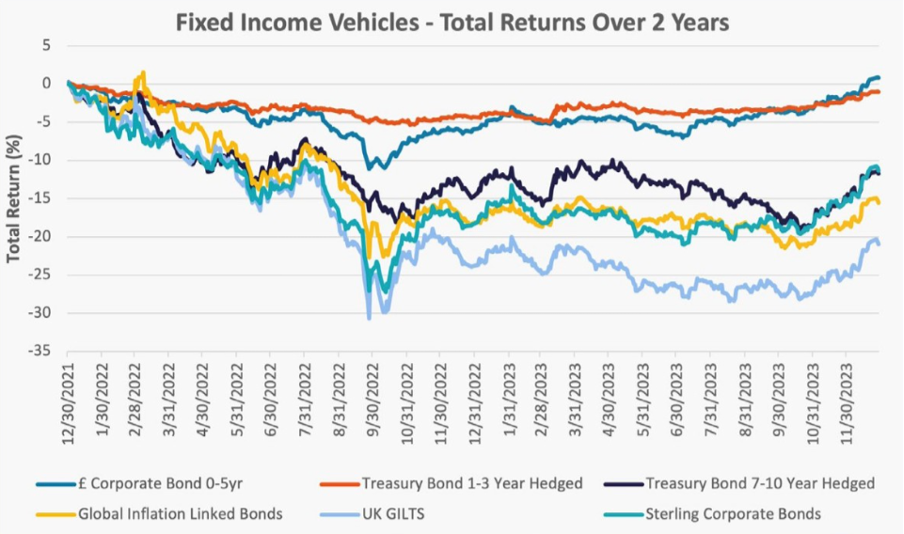

Longer duration bonds are more sensitive to shifts in interest rates, and this has been particularly evident over the past two years, with the capital value of the longest dated UK government bonds down more than 50% from their highs. For investors holding gilts as a ‘safe haven’ asset, this has been a perilous trajectory.

Source: Bloomburg, as at 31/12/2023

Active management of credit risk is also important. The credit spread reflects a premium paid to investors for taking on the higher risk of a corporate issuer versus a developed market sovereign issuer. At times, these spreads can be very generous and investors are well rewarded for bearing this risk, at others these spreads are tight and there is little pick up in expected return from moving out of sovereign bonds. The credit spread needs to compensate sufficiently for any expected deterioration in economic conditions.

We look at this spread and the ‘all-in-yield’, contrasting it with the expected returns from equity investments. Equities should, in theory, offer a higher return for sitting further down the capital structure and taking on greater risk. We will also examine the relative value between investment grade and high yield bonds.

Inflation is another variable. Some bonds have explicit inflation linkage and will move around with inflation expectations. These expectations have been extremely volatile in recent years and there have been periods where inflation-linked bonds have looked both well-priced and extremely expensive. We completely exited our inflation-linked position in 2022, believing inflation expectations had moved too high, before reinvesting in 2023. This was not a call on the top of realised inflation, but a view on the relative attractiveness of market pricing of future inflation.

Currency will also be a factor in our decision-making. While currencies are difficult to predict, currency exposure needs to be understood given it can be as big a driver of (or detractor from) the returns as the underlying investment itself.

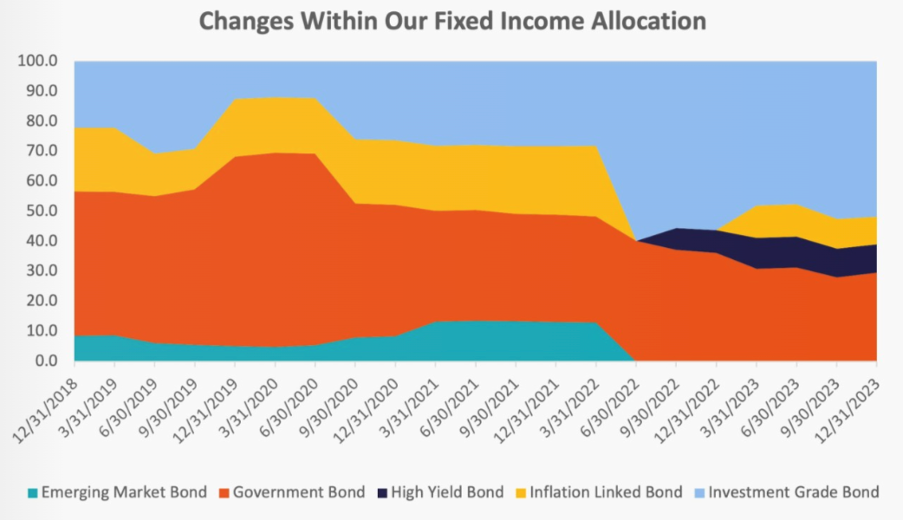

Source: Charles Stanley, as at 31/12/2023, Blended 2 MPS.

Strategic bonds?

It would be possible to hand these decisions to a strategic bond manager and let them flex these four factors to optimise risk and reward for clients. However, this approach comes with a number of inherent problems. The risk in strategic bond funds can vary considerably depending on their positioning at any given moment. At the extremes, a strategic bond fund could be all in high yield and emerging market debt at one point, and in short-dated developed market government bonds at another. At times this may be appropriate for an individual client, but a change in positioning may mean it no longer holds the required risk parameters.

Fixed Income positioning needs to be viewed in the portfolio context, not in isolation. Equity and alternatives can be sensitive to movements in fixed income yields which can remove diversification benefits if not anticipated. We believe a more nuanced approach is important.

Fixed income analysis

In assessing which levers to employ at different times, we assess the macroeconomic environment and prevailing market valuations. Our macroeconomic analysis is a natural part of our asset allocation work and will incorporate a vast range of inputs, including forward-looking economic growth considerations, inflation and interest rate analysis. On valuations, we are looking at the sovereign yield, any inflation compensation, the credit spread and the term premia to determine whether the risks and opportunities are fully reflected in market pricing.

For each position, we also need to decide whether to implement it through passive or active funds or through direct securities. Each approach will have its merits and it will depend on the end client’s objectives and investment parameters. The options within fixed income, particularly within passive funds, have grown significantly in recent years.

The selection of fixed income implementation options warrants as much attention as equity and alternatives when building portfolios. In our view, an active and targeted asset allocation is the best approach to capture the breadth of opportunities and risks within fixed income markets.

About Chris Ainscough

Chris is a Director of Asset Management, having joined Charles Stanley in April 2014. He is responsible for Charles Stanley’s range of open-ended UCITS investment funds as well as the Charles Stanley Blended MPS suite. Chris is a CFA Charterholder, holds the Investment Management Certificate, and has a Masters degree in Mathematics from Oxford University.

For more information on how Charles Stanley can partner with your business, contact Head of Strategic Partnerships, Tom Hawkins on 020 3627 3990, or click here to email.

The value of investments, and the income derived from them, can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable guide to future returns. Charles Stanley & Co. Limited is authorised and regulated by the Financial Conduct Authority.