For many investors it seems, gilts have become the new ‘gilty’ pleasure. But as record numbers of retail buyers pile into long-dated government bonds, could this craving turn unhealthy? Sharing his latest thinking with us below, industry veteran, Stephen Snowden, Head of Fixed Income at Artemis, weighs up whether it’s time for investors to swap their sweet spot in gilts for something a little more corporate.

Popular investment platforms such as Hargreaves Lansdown, AJ Bell and interactive investor are reporting record demand for gilts from customers. They’re not giving away numbers, but I believe the amount now owned directly by retail investors could run to billions.

It’s not surprising. Long-dated (30-year) gilts are currently offering yields of 5.25%, and if you buy them direct through these platforms the gains can be tax-free. This is an unusually generous tax perk. I don’t see it being removed while the government so desperately needs our cash, but it’s not guaranteed forever. While it remains – and given that CPI inflation is currently 3.8% – what’s not to love?

Markets are currently pricing the Bank of England base rate to be around 3.5% by the middle of next year. Textbooks tell us that falling interest rates are good for all bonds and for long-dated ones especially. So there’s potential for some capital uplift, too, though bear in mind that once bonds reprice the effective yield is lower.

But investors need to understand the risks of holding these gilts, including opportunity cost. Most developed nations are running large budget deficits in today’s environment, and that’s putting pressure further down the yield curve.

That 5.25% doesn’t look so attractive if you’re starting to get anxious about the government’s ability to repay the loan. That’s why institutional bond buyers are now in the driving seat on next month’s Budget. They’re telling Rachel Reeves that they’ll expect a lot more reward for lending if she doesn’t find an effective way to mend the deficit.

The capital value of existing bonds on the old terms may go down rather up if the government is forced to issue new bonds at significantly higher rates.

I’m not talking down the UK economy. It’s the government with the debt problem, not the consumer. Overall, consumer savings are incredibly high and debt relatively low. Companies have also been deleveraging – paying down their debt and issuing bonds at a much shorter maturity than historically (why would you lock yourself into higher rates for a long time if you think interest rates are coming down?).

Against this backdrop, you would expect credit spreads to be the tightest they’ve ever been in history. In simple terms, if government lending is getting more risky – and corporate lending less so – then the gap should narrow between what you typically get paid by the government and what, say, Tesco pays. It hasn’t.

Of course, there are risks with corporate bonds, too. Another Covid-type disaster might befall us. Individual companies might go pop. And, having worked with a woman whose father had his businesses nationalised 50 years ago, I know that governments have the power to seize a company’s assets at the stroke of a pen. So there’s a limit to how far spreads can tighten. But you can see how people might consider some corporates a safer bet than governments at the moment.

In my mind, that means the direction of travel is unquestionably towards tighter spreads – which makes buying corporate bonds now more interesting, if a little fraught. The Budget is once again creating massive uncertainty. It will do so for several more weeks. That could make things volatile, so you might want to wait till that’s blown over before investing – or you might want to be ready to jump at peak gloom, when the press is warning that the UK economy is going to hell so fast that the handcart has a motor.

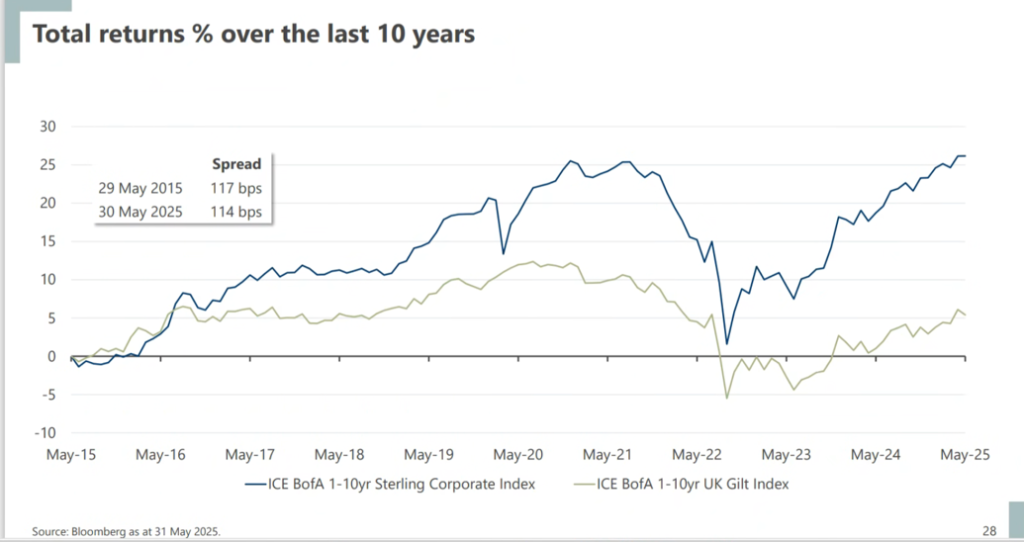

Now, let’s look at what investing in corporate bonds over gilts has done for investors over the long term. If I showed you a chart of the past decade you would see that £100,000 invested in gilts would have become £105,756 today[1]. The same amount in the 1-10yr Sterling Corporate index would have become £130,994. That would be disingenuous of me. A decade ago the world was panicking about oil at below $40 and growth concerns. Significant spread recovery fuelled a significant chunk of that corporate bond return. I don’t need to cheat to prove a point. The chart for the decade to May 2025 is fairer. It demonstrates starting spreads then not much different to today. The return comparison becomes £106,099 v £126,045. And I like to think that with good active management it would have been more still.

Yes, the corporate bond journey is more volatile, but these bonds generate more income and this compounds – that’s what drives the strong returns.

I’m not a financial planner, but my thinking is that gilts make most sense outside a tax wrapper like an ISA or a pension as a substitute for a bank deposit. But within these wrappers, where the tax-efficiency advantage of gilts is removed, corporate bonds should be more appealing. And if investors aren’t using their ISA allowances, preferring the gilt option instead, they risk missing out.

That ‘gilty’ pleasure could prove a costly one to them over time.

Stephen Snowden is Head of Fixed Income at Artemis