‘Riskier’ assets

Inflation normally occurs for two reasons.

One is scarcity: in times of economic booms, companies can struggle to find workers and resources to cope with demand, wind up paying more to obtain them, and then raise prices to meet these increased costs.

The second is currency debasement – when governments print more money, the value of the money its citizens have been saving falls.

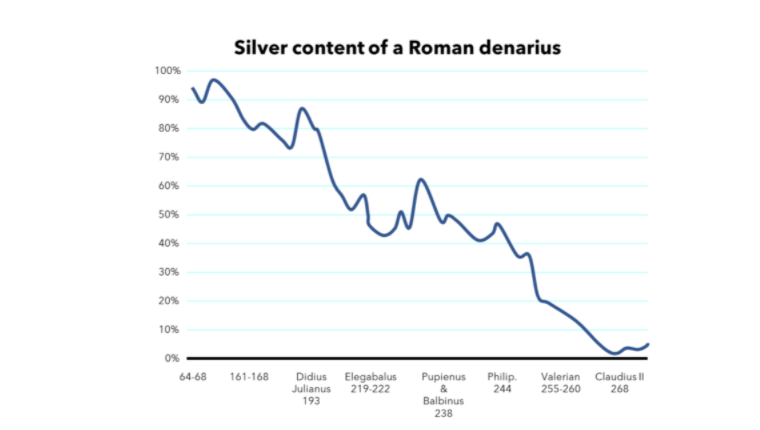

Here, in one of our favourite graphics, you can see how the silver content of a Roman denarius fell as the rulers of the Empire debased the coins to fund expansion. Evidently, a denarius bought far less in AD268 than it did in AD64…

Source: Tulane University, Société Générale

Whereas modern methods of injecting money into an economy – such as quantitative easing – have more nuance than those used by the Romans, they too can lead to inflation if the increase in monetary mass finds its way into the economy.

When considering ultra long terms, it pays to consider riskier asset classes, if the expected long-term return is appropriate to the risk taken. This is because the effects of compounding at a higher rate will help to meet the higher costs of living brought on by inflation.

Sticking to low-risk, low-return assets – such as fixed income – is unlikely to be sufficient to meet those future expenses.

Diversification

There are of course three important footnotes to this, which underline the importance of advisers regularly reviewing their clients’ needs.

Firstly, some clients receive an income that is less predictable, so may be attracted to asset classes with more predictable short-term returns.

Secondly, as clients approach retirement, they may have both short- and long-term liabilities, and their asset mix should reflect that.

Finally, people may prefer less volatile asset combinations because of their financial personality.

Then there are the benefits of diversification.

Mixing assets has the advantage of reducing risk to a greater degree than its reduction in return. This is because asset classes are not perfectly correlated and react differently to various market conditions. By not sitting exclusively in one or the other asset class, investors can smooth their return stream and receive a diversification benefit.

In summary

Saving is an asset-liability puzzle. A client’s portfolio should reflect life’s uncertainties and how able they are to endure certain levels of risk.

Investments based on real assets (equities, commodities) tend to be more volatile in the long term than those based on nominal assets (cash, government bonds), but also provide a better hedge against inflation.

Education is essential: clients should be aware that (i) the future will arrive, (ii) they will need to fund it, and (iii) putting money in low-risk assets may not achieve that objective.

Finally, diversification is a powerful tool to reduce expected risk in a way where less expected return is sacrificed in the trade-off, improving the expected remuneration per unit of risk.

Thomas Rostron is chief executive of Horizon by Embark