Written by William Macleod, Managing Director at Gravis Advisory Limited

In 2013, during the postmortem of the global financial crisis (GFC), a new European directive entitled the Alternative Investment Fund Managers Directive (AIFMD) was introduced. The aim was to regulate alternative investments such as hedge funds and private equity funds – products considered to be too lightly regulated at the time – and to protect EU economies from systemic risk. A sensible move, you’d think.

Inexplicably, however, Investment Trusts (now referred to as Investment Companies) were included in this legislation – even though they were listed on the London Stock Exchange and already highly regulated under UK Listing Rules and the pre-existing corporate and regulatory framework. Roll on a few years and the introduction of successive directives in Europe including PRIIPs and MiFID II now mean that the Investment Company sector is increasingly over legislated.

The result of this over legislation has been that some Investment Company costs are double counted, leading many pension and institutional investors to sell their holdings rather than reflect higher costs in their reporting to clients. Those that have not, have suffered huge client withdrawals because they now appear to be artificially expensive thanks to the duplication. For want of a better word, it’s bonkers.

The double-counting explained

Investment Companies are like any other public company. Their share prices reflect the market’s assessment of their value based on all their disclosed financials, including fees paid to their managers. As such, the share price discounts the costs and investors’ value is represented by the price at which the shares are bought and sold. Full disclosure of all costs is therefore imperative and a high level of transparency through regular reporting is essential and welcomed by industry participants.

However, given that Investment Companies’ share prices already reflect the value of a company based on this high level of cost disclosure, it makes no sense to require institutions and advisors who invest in the shares of Investment Companies to report the costs again in their own disclosures to their clients. This is the double counting I’ve referred to and its requirement reflects a misunderstanding of the nature of a listed investment and impact of fees on the investment (i.e., the share price).

Why does this matter?

The 369 LSE listed Investment Companies have combined assets exceeding £256bn and provide critical support for financing schools, hospitals, transport, renewable infrastructure, battery storage, the airline and shipping industries, industrial warehousing, student accommodation, retirement homes, affordable private rental housing, as well as venture and growth capital to entrepreneurial UK firms.

The sector is a UK success story and provides an easily tradeable way for investors to hold otherwise illiquid assets, generating returns for themselves while supporting critical parts of the UK economy.

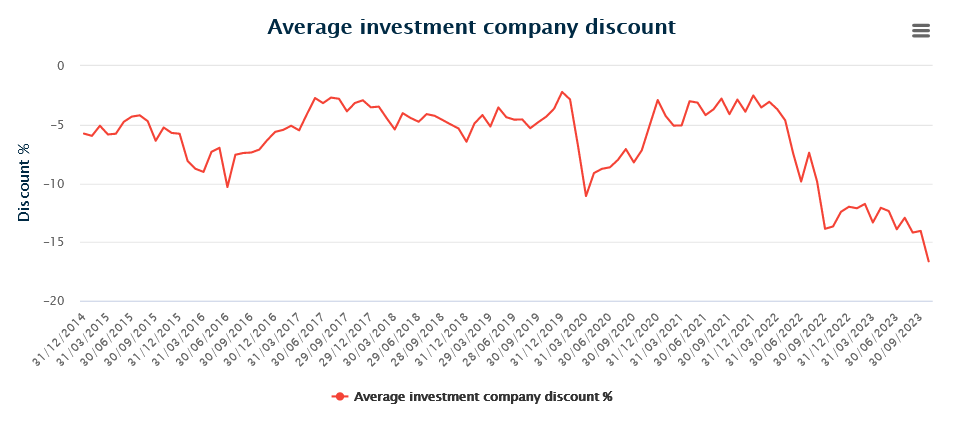

When there are more sellers than buyers, prices tend to collapse. And that is exactly what has happened. The chart below shows the extent to which prices have declined, relative to the underlying value of the companies. According to the Financial Times, these discounts are wider than in the immediate aftermath of the GFC.

Source: The Association of Investment Companies

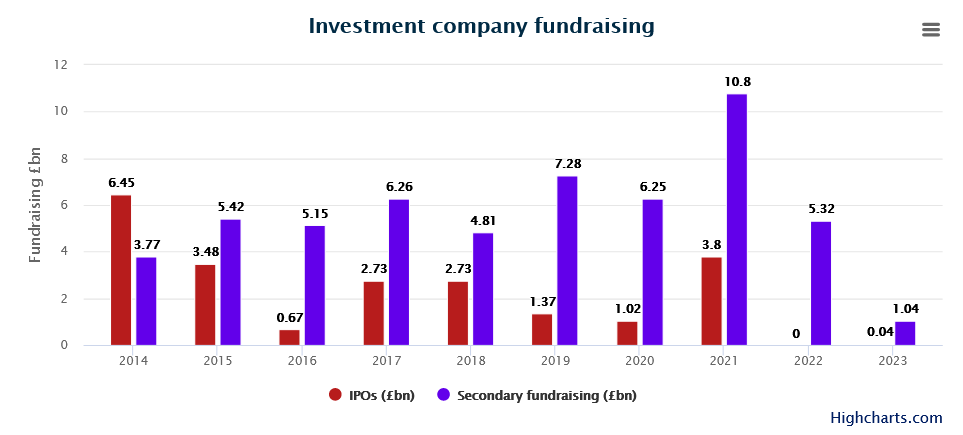

What’s more, financing looks as though it has dried up in the wake of the cost disclosure requirements.

Source: The Association of Investment Companies

Yes, there are other factors at play. The macro shift as interest rates have normalised has had a big impact. So too have recession, geo-political risk, over-issuance, and some recent high-profile corporate governance failures.

But there is now ample anecdotal evidence that this double counting is having a fundamental impact and will have damaging long-term consequences for the Investment Company sector – even in a more benign environment.

What is the solution?

Removal of Investment Companies from AIFMD would immediately eradicate this problem. Baroness Altmann has proposed a Private Members Bill to this effect that will be heard on 22nd November 2023. She has also raised the subject in the House of Lords on 13th November 2023.

The Investment Company sector is not out of the woods yet. But with the right backing, a simple change could clear the path for a recovery and a new lease of life for a critical part of the UK’s financial ecosystem.

![[UNS] celebrate](https://ifamagazine.com/wp-content/uploads/2024/11/jason-leung-Xaanw0s0pMk-unsplash.webp)