Written by Gaël Fichan, head of fixed income at Syz Group

The recent announcement of a snap election in the UK on July 4th has sparked discussions about its impact on both the political landscape and financial markets, particularly the Bank of England’s (BoE) monetary policies.

Context

Prime Minister Rishi Sunak’s decision to hold elections earlier than anticipated, opting for July rather than January, seems driven by a mix of political and economic considerations. Despite the April Core CPI aligning closely with the Bank of England’s target at 2.3%, potentially marking a tactical victory for Sunak, the Labour party is still favoured to secure a significant parliamentary majority according to current polls and recent local and by-elections. However, the constraints on fiscal policy due to limited budget flexibility suggest that regardless of the election’s winner, significant shifts in fiscal policy are unlikely. This scenario implies that the election will have minimal impact on the BoE’s immediate monetary policy direction, except perhaps delaying a rate cut until August rather than June.

Market Implications

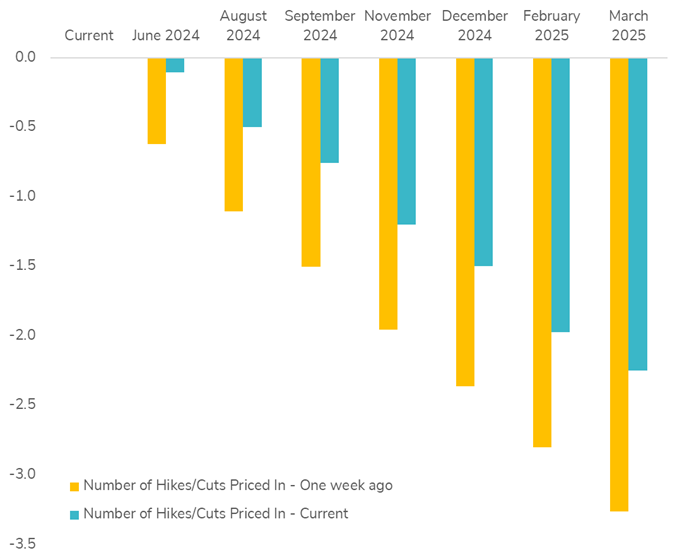

The recent release of UK inflation data showed progress but fell short of market expectations. Core inflation, excluding food, fuel, alcohol, and tobacco, remains high at 3.9%, compared to the previous month’s 4.2% and against a market expectation of 3.6%. Meanwhile, services inflation stands at 5.9%, nearly unchanged from the previous month and above the expected 5.4%. This persistent inflationary pressure has led markets to drastically lower expectations of a Bank of England rate cut at its upcoming meeting, from a 60% probability last week to just 10%.

Interest Rate Probability for BOE: Current vs One week ago

Despite the political context, historical precedents indicate that the BoE is likely to proceed with its planned Monetary Policy Committee meeting on June 20 without significant alterations. This consistency in past behaviour during election periods underscores that the Bank’s decisions will continue to be guided by economic data rather than political developments. Nevertheless, with the latest inflation figures, the BoE has all the economic justification it needs to possibly wait until August before adjusting its monetary policy.

However, the market reaction was quite pronounced in rates; the 10-year UK yield jumped by 10 basis points, while the front end of the Gilt yield curve surged by 15 basis points to 4.45%. The UK yield curve remains inverted, with the gap between the 2- and 10-year UK yields narrowing to -20 basis points, the lowest level since March.

Conclusion

In conclusion, the decision to hold a snap election in the UK does not appear poised to dramatically alter the landscape of monetary policy in the short term, despite its potential implications for the political scene. Prime Minister Rishi Sunak’s strategic timing—prompted by moderately encouraging inflation figures and political pressures—suggests a calculated move to preempt worsening economic conditions that could further complicate governance.

While the Labour party is projected to secure a robust majority, the limited fiscal flexibility and enduring high core inflation mean substantial policy shifts are unlikely, regardless of the election outcome. Consequently, this political event is expected to have a minimal direct impact on the Bank of England’s monetary policy decisions, which are anticipated to remain data-driven.

The financial markets’ immediate reaction, notably in the Gilt market, underscores the sensitivity to ongoing inflation concerns and anticipates a cautious approach from the BoE with potential rate adjustments not expected before August. Overall, while the election introduces a new variable into the mix, the foundational economic policies guiding the BoE’s actions remain steadfast, anchored by prevailing economic conditions rather than the shifting political winds.