With fewer bonds beating inflation, savers risk missing out unless they act quickly to secure rates. Moneyfacts reveals the state of play in the fixed bond market for savers.

Fixed bond rates showed a mixed picture this month, with some terms seeing slight increases while others held steady. The top two- and three-year fixed bonds increased, while the top one-, four-, and five-year bonds remained unchanged.

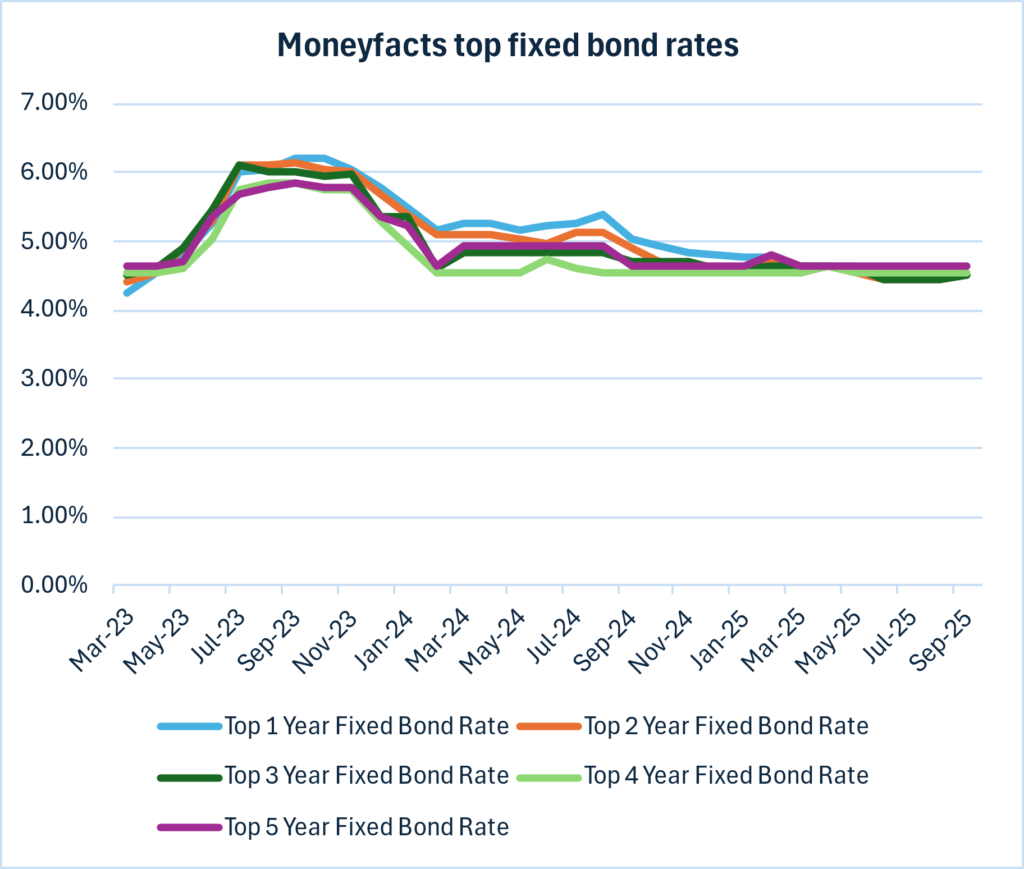

The leading one-year fixed bond held at 4.50% gross, which is 0.14% lower than the top five-year fixed bond at 4.64%. A month earlier, the five-year bond rate was also higher than the one-year by 0.14%. In March 2025, the gap between the top one- and five-year bonds was just 0.06%, with rates of 4.58% and 4.64%, respectively. A year ago, the top one-year bond offered 5.05% compared with 4.64% on the five-year, creating a wider gap of 0.41%.

| Savings market analysis – top fixed bond rates | |||||||

| Mar-23 | Sep-23 | Mar-24 | Sep-24 | Mar-25 | Aug-25 | Sep-25 | |

| Top one-year fixed bond rate | 4.26% | 6.20% | 5.26% | 5.05% | 4.58% | 4.50% | 4.50% |

| Top two-year fixed bond rate | 4.40% | 6.13% | 5.10% | 4.90% | 4.53% | 4.44% | 4.50% |

| Top three-year fixed bond rate | 4.50% | 6.00% | 4.85% | 4.72% | 4.63% | 4.44% | 4.50% |

| Top four-year fixed bond rate | 4.53% | 5.85% | 4.54% | 4.54% | 4.54% | 4.54% | 4.54% |

| Top five-year fixed bond rate | 4.63% | 5.85% | 4.95% | 4.64% | 4.64% | 4.64% | 4.64% |

| Top interest rates based on a £10,000 deposit as at the start of the month. | |||||||

| Source: Moneyfactscompare.co.uk | |||||||

Looking at the longer-term trend in the savings market, the top one-year fixed bond has fallen from 6.20% in September 2023 to 4.50% by September 2025. The top two- and three-year bonds followed a similar path, peaking in September 2023 at 6.13% and 6.00%, respectively, before declining to 4.50% each by September 2025. The four-year fixed bond has held steady at 4.54% since March 2024, while the five-year fixed bond has remained unchanged at 4.64% since September 2024. These top rates are based on a £10,000 deposit as of the start of each month, according to Moneyfactscompare.co.uk.

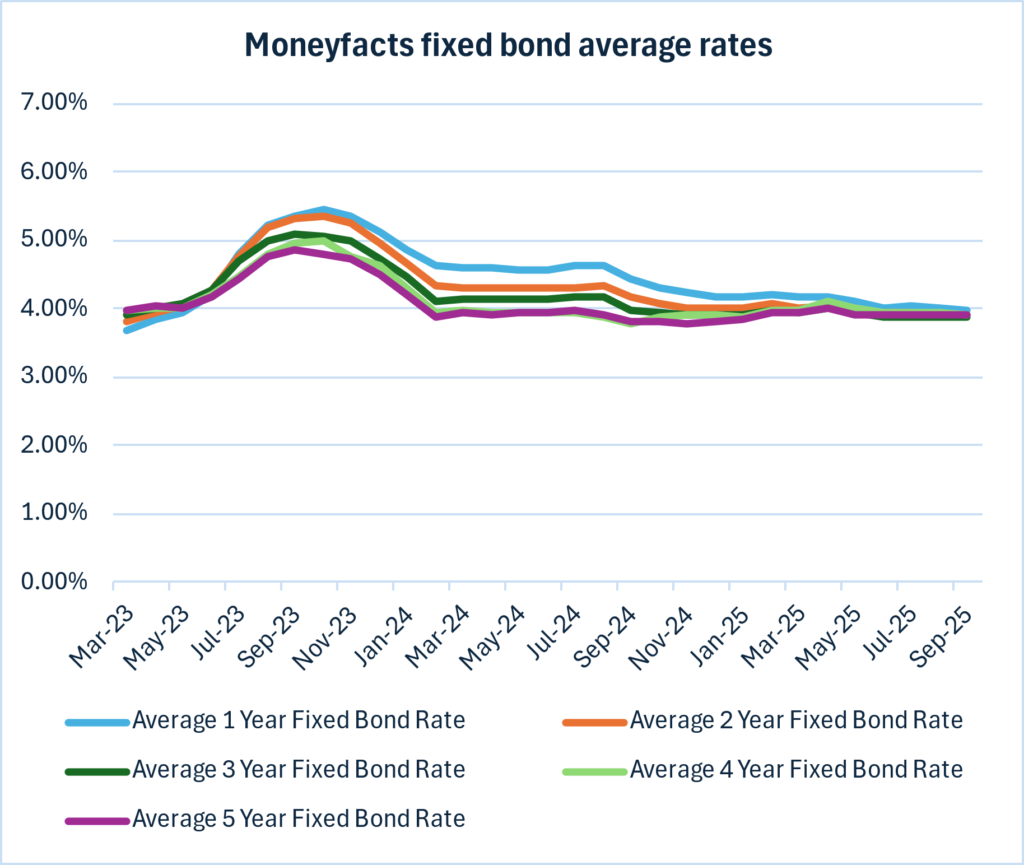

On average, the one-year fixed bond rate at 3.97% gross is now 0.05% higher than the five-year average at 3.92%, narrowing from a 0.10% gap the previous month. Back in March 2025, the rate difference was wider, with the average one-year bond at 4.16% and the five-year at 3.96%, a gap of 0.20%. A year ago, the average one-year bond returned 4.43% compared to just 3.80% on the five-year, marking a significantly larger gap of 0.63%.

| Savings market analysis – average fixed bond rates | |||||||

| Mar-23 | Sep-23 | Mar-24 | Sep-24 | Mar-25 | Aug-25 | Sep-25 | |

| Average one-year fixed bond rate | 3.69% | 5.35% | 4.61% | 4.43% | 4.16% | 4.01% | 3.97% |

| Average two-year fixed bond rate | 3.81% | 5.32% | 4.31% | 4.19% | 4.02% | 3.91% | 3.90% |

| Average three-year fixed bond rate | 3.92% | 5.09% | 4.15% | 3.99% | 3.96% | 3.87% | 3.89% |

| Average four-year fixed bond rate | 3.99% | 4.97% | 3.97% | 3.77% | 3.99% | 3.94% | 3.90% |

| Average five-year fixed bond rate | 3.99% | 4.86% | 3.94% | 3.80% | 3.96% | 3.91% | 3.92% |

| Average interest rates based on a £10,000 deposit as at the start of the month. | |||||||

| Source: Moneyfactscompare.co.uk | |||||||

Caitlyn Eastell, Spokesperson at Moneyfactscompare.co.uk, said:

“Inflation-beating fixed bonds take up just one quarter of the savings market. Over the past month the number of fixed bonds paying above inflation has fallen by over 100, and with further spikes expected, savers may find it increasingly harder to find an attractive deal. Adding to the struggle, many of the top bonds pay less than 1% in real terms.

“Despite the cut to base rate last month, the top rates have remained solid, some even saw small increases. However, on average savers will now receive less than 4% across all fixed terms, the last time this was the case was March 2023.

“Two years ago, the short-term market-leading rates peaked at over 6%, at the time these were the highest since 2008. Those savers who were lucky enough to secure a top deal and deposit £10,000 could now be enjoying over £1,000 in interest. However, if they decide to reinvest today, due to tumbling rates, they will earn almost £350 less by the time their two-year term ends. It is crucial that savers are not deterred, as many fixed bonds are still very competitive and choosing not to do anything could leave them significantly worse off.”