Royal London’s research into workers’ retirement savings habits shows that pension contributions differ significantly by age, job type, and income. The one consistent is that the gender pension gap impacts women at every stage of their career, leaving them worse off in retirement.

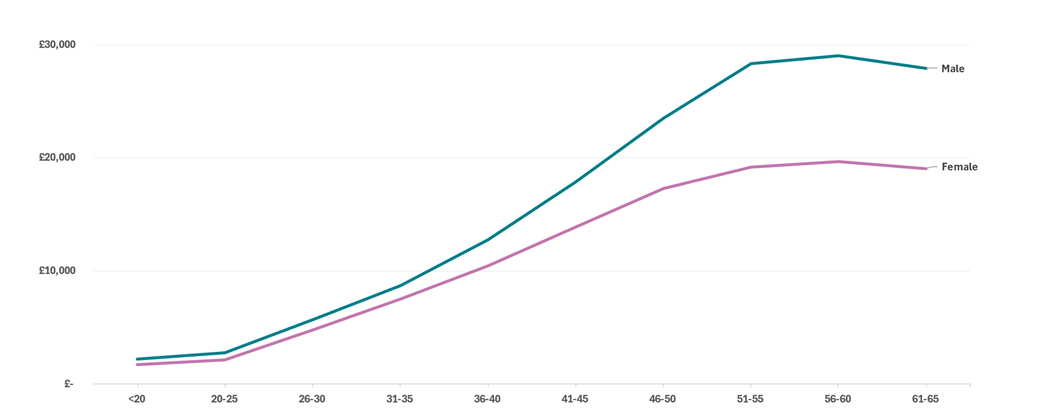

The level of contributions workers and their employers make affects the lifestyle they will enjoy in retirement. And despite near parity in pension participation rates between the sexes, data from nearly two million customers saving with Royal London shows that, compared to men, women typically save less for their retirement throughout their working lives, with a gap of 16% in their 30s rising to 43% by the time they reach age 55*.

Average workplace pensions savings by age for men and women

While there was once a perception that women were less likely to engage with their pension, the narrative has changed. Royal London’s research** showed that when it comes to the importance placed on pensions as a workplace benefit, there is no gender difference. In fact, women are more likely than men to put pensions at the top of their wish list when applying for a new job.

The financial impact of parenthood and caring on women’s pensions

One of the main factors responsible for the gender pensions gap is the different working patterns between men and women. Many women take on lower paid part-time jobs to allow them to juggle employment and looking after others. And, significantly, around one million women below age 50 don’t work due to caring responsibilities^.

It’s an issue that disproportionately affects women. Figures from the Office for National Statistics (ONS)^^ show that older female workers are also twice as likely to take on caring responsibilities, which comes at a cost to their retirement savings.

Employer Matching: A missed opportunity for many women

Many employers offer valuable pension matching, so it’s encouraging that, overall, two-fifths** of workers put more than the standard amount into their pension each month to take advantage of employer matching. However, there is a clear imbalance between the sexes with more men than women taking advantage of employer matching contributions (48% versus 41%). Importantly, affordability is a barrier for half of women, compared to 39% of men who cite this as the reason for not using employer matching.

Clare Moffat, pensions expert at Royal London, said:

“Millions more women may now be saving thanks to auto enrolment, but we can’t escape the fact that parenthood and caring responsibilities interrupt women’s working lives. It’s an issue that affects their take home pay, career opportunities and ultimately their pensions savings.

“The decisions taken about stepping back from work, or reducing hours to care for children, have such significant implications for the future that it’s worth considering all the options. It’s not that a different decision would be reached, but many women look back and wish they’d known more at the time about the actions they could have taken.

“At the start of people’s career, there’s not much of a difference in the pension savings between men and women, but the effect of having a family and reducing their hours means the gap widens significantly as time goes by. So, at the point of retirement, women typically only have around £60 saved for every £100 that men have.

“And on top of that, on average, women live longer and therefore have longer retirements, so rather than less savings, they actually need more money for their retirement than men.

“It’s also nice to put the myth to bed that women are less interested in pensions. A move that hopefully shows greater empowerment and control of their long-term finances.”

Top tips to overcome gender saving barriers

- The best preparation for your long-term future is to start saving as early as you can. Saving for retirement as soon as you start working, and before you start a family, enables small amounts of money to grow into larger sums over time.

- Review your pension savings regularly, at least once a year. As well as showing how much is in your pension, it will also let you know if you are on track for the retirement you want. Understanding how much you need in retirement is important. The PLSA’s Retirement Living Standards can help with this. Discovering any potential shortfall sooner can give you time to take action to improve your lifestyle in retirement.

- When you get a pay rise, try and allocate some or all of the extra money into your pension.

- Investigate whether your employer offers pension contribution matching, allowing you to maximise your savings. Increasing your regular pension contributions using matching, if you can afford to, will really boost your pension.

- Make a retirement plan. Not being prepared for retirement can cause a number of issues in later life. Think about when you want to stop work and, crucially, how you’ll spend your time when you retire. For example, if you enjoy meals out and weekends abroad now, will you be able to do the same in retirement? That will make it easier to work out how much retirement will cost you.

- You don’t have to do it alone, there’s plenty of guidance and advice available. Your pension provider may offer tools and calculators. Managing your pension can feel complicated. Does your employer offer sessions with a financial adviser to explain how your pension works? Learning to understand more about pensions will give you more confidence. Expert financial advice on your pension savings and especially for those nearing retirement is recommended. There’s also lots of information and guidance at the independent and government-backed MoneyHelper website. For more information on the help you need, tailored to your current circumstances, visit this page from Royal London.

- If you are part of a couple, then plan for retirement together. Contributing to a spouse’s or partner’s pension and ensuring you’re both maximising the State Pension entitlement are among the steps you can take to ensure you’re retiring together in the style that you deserve.