When looking at historical inflation-adjusted performance of a number of asset classes, real assets have typically performed well in reflationary conditions (unsurprisingly), as well as in stagflation—historically a challenging environment for both stocks and bonds. Additionally, commodities and resource equities are generally the most sensitive to upside inflation surprises, regardless of the growth backdrop. Real estate has been somewhat less geared to inflation trends and more tied to economic growth than commodity-linked real assets, while infrastructure has been fairly consistent across all regimes, including greater resilience in stagnation than other equity categories.

Differentiated responses to growth and inflation surprises demonstrate the potential of real assets to enhance portfolio stability over full economic cycles, potentially helping to offset periods that may be more difficult for generating attractive returns through stocks and bonds.

Strong total returns

Real assets have historically generated strong returns over full market cycles, with all but commodities delivering performance in line with or better than global stocks over the past 50 years. The long-term average for commodities has been depressed by a decade-long bear market from 2008 to 2018, driven by the downshift in China demand and an oversupply cycle. However, commodities have since experienced substantial improvements in supply/demand fundamentals and a more supportive macroeconomic backdrop, providing potential catalysts for a sustained multi-year recovery.

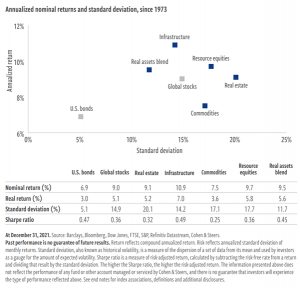

Furthermore, combining multiple real assets within a single portfolio may offer additional benefits. A diversified real assets blend has historically delivered competitive returns with significantly less volatility than global stocks or standalone real assets, capitalising on diversification benefits available within and among the different real assets categories.

Exhibit 2: Combining real assets may improve risk-adjusted returns

Investors’ approach to real assets depends on their objectives

Historically, no single real asset has excelled across each of the criteria of inflation sensitivity, diversification potential and total returns. Some real assets have historically performed better on certain dimensions than others, requiring investors to consider various strengths and trade-offs according to the specific role of real assets in their portfolio.

Strategic inflation defence at attractive relative value

As investors consider how to best protect against the risk of higher inflation, history shows that including real assets in a portfolio may provide key benefits, including the potential for inflation sensitivity when needed, attractive risk-adjusted returns over full market cycles and added benefits from diversified real assets exposures.

Moreover, the repeated and unprecedented disinflation surprises of the 2010s weighed on real assets returns while the broader market surged to ever-higher levels. This has resulted in historically attractive real assets valuations relative to equities, even after the group’s strong returns in 2021.

We believe this combination of potential inflation benefits, diversification and relative value represents a compelling opportunity to realign portfolios to take advantage of what real assets can offer.