Written By Laith Khalaf, head of investment analysis at AJ Bell

The market is a pretty grisly place to be right now, as high inflation, rising interest rates, and economic pessimism have taken their toll on sentiment. The MSCI World Index is down 9% this calendar year in sterling terms, and it feels like there’s no place to hide from the current malaise. One area that’s been doing better than most though are equity income funds which invest predominantly in dividend-paying shares.

As the performance table below shows, so far in 2022 equity income funds have held up a lot better than other areas of the market. This is a significant reversal of fortunes, especially for the UK Equity Income sector which has been a real laggard until this year.

Selected major equity fund sectors

| Total return | ||

| Sector | 5 years to 31/12/2021 | 2022 Year to Date |

| IA Global Equity Income | 51.1 | -3.8 |

| IA UK Equity Income | 26.4 | -4.4 |

| IA North America | 97.8 | -9.0 |

| IA Japan | 41.8 | -10.3 |

| IA UK All Companies | 36.4 | -10.5 |

| IA Global | 77.8 | -11.7 |

| IA Global Emerging Markets | 44.1 | -12.1 |

| IA Europe Excluding UK | 58.3 | -14.3 |

| IA UK Smaller Companies | 84.2 | -19.1 |

Source: FE, total return in GBP to 9th May 2022

Returns from the Equity Income sectors have still been negative this year, but in a falling market, some downside protection is not to be sniffed at, and shallower price falls means these stocks have less ground to make up when sentiment turns. There are also good reasons to believe that equity income funds could be set to come back into fashion, after a long period out in the cold.

Dividends are one in the hand rather than two in the bush

A number of factors explain why equity income funds have been doing better than other sectors of late. Technology stocks have sold off heavily, and some of the big names in this area like Alphabet, Amazon and Meta, don’t pay a dividend, so would rarely find themselves in equity income portfolios. Energy stocks on the other hand, tend to be big dividend payers, and we have seen their value rise as oil and gas prices have spiked.

Inflation and rising interest rates have also made one in the hand look more attractive than two in the bush, which favours dividend paying stocks over those that reinvest for future growth. Neither of these macro-economic factors look like disappearing any time soon. All of that has also helped the FTSE 100, which comes packed with old economy dividend payers, perform better than most markets this year

No-one knows if current trends will continue or if the global market will recover in the not too distant future. The tech-heavy US stock market has fallen by over 15% this year, but valuations still look high by historical standards, even though they are more modest than they were.

If we are entering a period of market falls, or stagnation, some equity income exposure could be a useful tonic for a portfolio. These funds are by no means exempt from downturns, but they may fare better than other areas of the market.

Partly that’s because the immediacy of a dividend provides a bit of a safety net when it comes to valuing a stock, as a cash payment will always set a floor as to what a share is worth. If the market knows XYZ plc is going to pay somewhere in the region of a 50 pence dividend per share, there’s a level below which the stock is unlikely to fall, because that income stream simply becomes too attractive to resist.

For instance, at a price of £5, XYZ plc is paying a yield of 10%, which is an extremely attractive level of income, and buyers are likely to be lured in well before it falls to that price.

Dividends recover from downturns, growth stock valuations may not

Of course, dividends can be cut too, and in the current environment where companies face higher debt interest payments, inflationary costs, and a weak economic outlook, dividends could come under pressure. This is definitely a risk for equity income funds, particularly seeing as many of the big dividend companies are cyclical businesses like mining companies and banks.

But the one thing we can say with some certainty about the global economy, is that if it falls backwards, it will recover. The same goes for company earnings, and dividends, which should rise over time.

By contrast, if the lofty valuations on some growth stocks are felled by rising interest rates, there’s nothing to say they will reach the same heady heights again. There are those who will say that the rapid changes we have seen in technology justify permanently higher valuations for the big monopolies providing digital services. But ultimately, stock valuations tell us what profits investors are willing to accept for investing in shares. It seems logical to conclude that the reason they have been willing to accept so much less in recent years is actually because the alternatives, cash and bonds, have been yielding next to nothing.

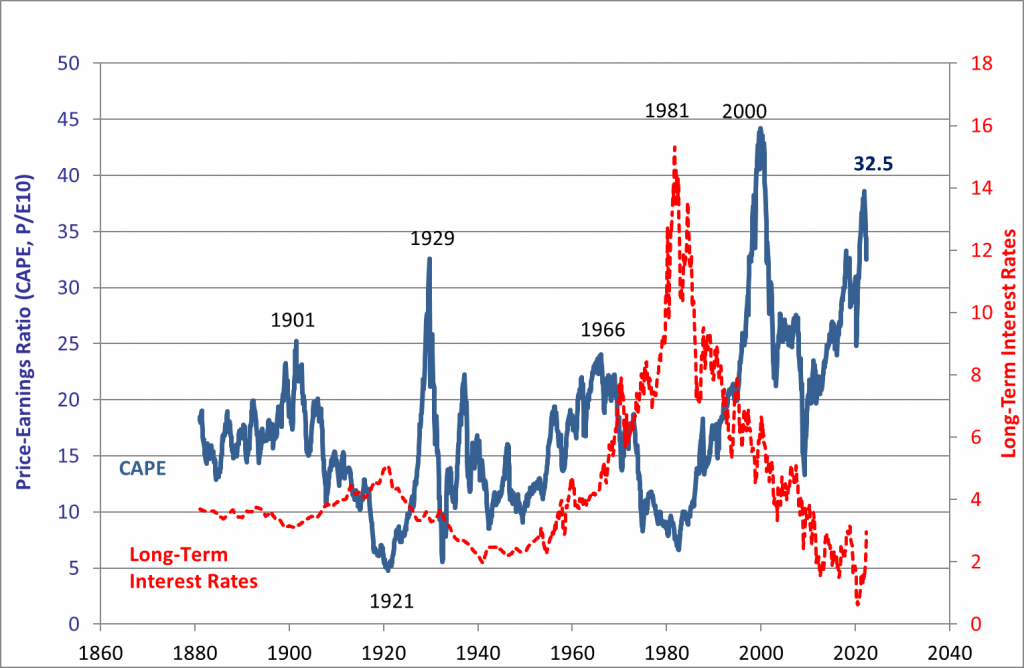

But that tectonic plate is now shifting quite rapidly, and as interest rates rise, the tide is seeping out on growth stock valuations. That tide may not regain its high water mark again, unless we see central banks moving back to near zero interest rates, or we experience a speculative market mania like in 1999. The Shiller CAPE ratio shows how stretched valuations have become in the US, and some may say this already points to an irrational bubble in stocks. Another view is that the bubble is entirely rational, a natural reaction to low cash and bond rates, but which will nonetheless deflate as monetary policy tightens.

Shiller US Cyclically Adjusted Price Earnings (CAPE) Ratio

Source: http://www.econ.yale.edu/~shiller/data.htm

Dividend cover is at its highest level since 2012

We should also bear in mind that there was a widespread dividend cull when the pandemic hit, as companies sought to cut their cloth to more constrained economic circumstances. This put dividend payments on a more affordable footing. One measure of this is dividend cover, which shows the ratio of company earnings to dividends.

Dividend cover for the FTSE 100 is now at its highest level since 2012, as the chart below shows. In 2022, dividend cover is now seen rising to 2.09 times, compared to an average of 1.5 times in the five years leading up to the pandemic (so companies are forecast to earn 2.09 times as much in profits as they pay out in dividends).

Clearly analysts can get their numbers wrong, and an economic slowdown means lower earnings, but even allowing for some downward revisions, that’s still a reassuring buffer against swingeing dividend cuts.

FTSE 100 Dividend Cover

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

Reinvested dividends buy cheaper shares in falling markets

Equity income isn’t just for income seekers either, because dividends can be rolled up and reinvested to produce a higher total return. Even in falling markets you’re getting some benefit from this approach because the cash dividends are being used to buy shares at lower prices. Consider that the headline FTSE 100 doesn’t include dividends, and is still only 4% higher than its 1999 peak.

But with dividends reinvested, the index has returned 131% for investors. In other words, £10,000 invested in December 1999 would be worth £23,100 today, with dividends reinvested.

Equity income funds and trusts to invest in

Investors can build their own portfolios of dividend-paying stocks, or invest through equity income funds which provide instant diversification. Investment trusts can be particularly useful for those looking to receive a regular income, as they can smooth dividend payments by building reserves back in the good years to pay out in the bad years.

One of the attractive things about the UK stock market is the level of yield it provides, and there are plenty of domestic fund and trust options available to investors, such as Threadneedle UK Equity Income (historic yield 3.1%) or City of London trust (yield 4.9%). While other areas of the global market tend to be lower yielding, investors should consider using them to build some regional diversification into their equity income portfolio, through funds such as Schroder Global Equity Income (yield 3.5%), Blackrock Continental European Income (yield 3.2%), or for more adventurous investors, Jupiter Asian Income (yield 3.8%).

As ever, it’s important not to over-expose your portfolio to one style of investing, but given the relatively lacklustre performance of equity income in recent years, combined with fund outflows from the sector, investors might find they could do with a greater allocation to this area.