By Rufaro Chiriseri, Head of Fixed Income for the British Isles at RBC Wealth Management

Subdued economic growth and troublingly persistent inflation suggest the UK may well fall victim to stagflation in 2024 if the labour market deteriorates further. The Bank of England is unlikely to be willing to cut interest rates before the second half of the year, in our view. Despite the unpalatable macroeconomic backdrop, we see opportunities for patient investors. We have a bias for UK bonds towards adding further to Gilts and increasing duration in the near term.

The window of opportunity in fixed income appears fully open.

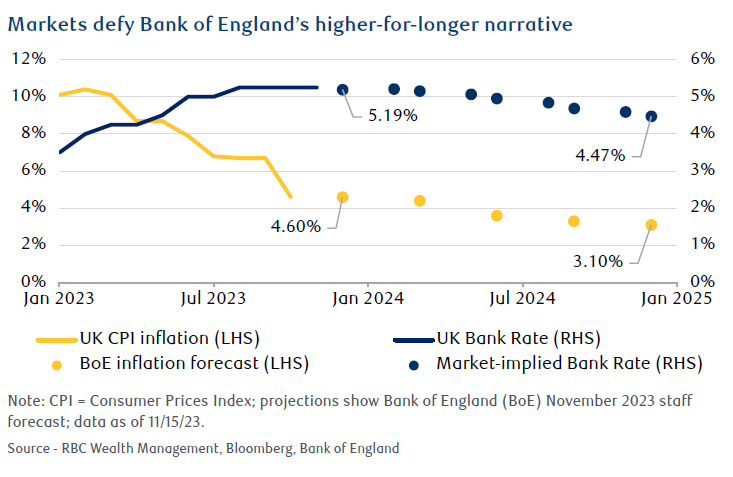

The question for bond investors is not how much more will the Bank of England (BoE) hike interest rates, but rather when will the first rate cut come through to propel bond returns. Our base case is no rate cuts through H1 2024 due to still stubbornly high inflation and wage growth. The Monetary Policy Committee (MPC) is likely to keep its hiking optionality, but we think the bar remains high for further hikes and 5.25% is likely the peak for this cycle. The market currently expects around 75 basis points (bps) worth of cumulative cuts to reach 4.56% in Q4 2024.

Inflation will likely meet the BoE’s Q4 2023 estimate, but this is still far from its 2% target. The November Monetary Policy Report utilised the market pricing in October which showed the Bank Rate at 5.25% throughout 2024. In this scenario, inflation only falls below target in Q4 2025, with a caveat of upside risks to this estimate—this heightens our conviction of no rate cuts in H1 2024. If there are any large and persistent surprises in inflation or wage data which exceed the MPC’s forecasts, the policy reaction would likely be to keep rates elevated for longer to maintain restrictive financial conditions, albeit at the expense of economic growth. The risk to our view of no rate cuts in H1 stems from the deteriorating growth outlook and the mortgage refinancing headwinds further hampering consumer demand, which could cool inflation faster than we expect.

Though the UK economy has fared slightly better than we anticipated, the outlook for growth is broadly flat for the next 12 to 18 months and the risks of a recession remain high, in our view. RBC is forecasting growth to stall in Q1 2024 at 0% q/q and mildly recover in the following quarters to reach a meagre 0.1% y/y in 2024.

Turning to Gilt supply, officials are reducing the BoE’s balance sheet (otherwise known as quantitative tightening) at a pace of £100 billion over a 12-month period, which has been priced in by markets. According to a recent government report, public finances have performed better than initially forecast in March, resulting in a lower borrowing requirement this fiscal year. RBC expects a £20 billion reduction in Treasury Gilt issuance to reach around £218 billion in gross supply this fiscal year. Gilt demand remains robust, but we are monitoring for signs of waning demand at future bond auctions, which could send yields higher. We have a bias towards adding further to Gilts and increasing duration in the near term.

Credit markets held up better than we expected in 2023, but it is not clear to us how much longer this “goldilocks” period will last. On a one-year basis credit spreads look wider, but they are nearer to fair value over a five-year period. Consequently, the risks that spreads will widen are still high, in our view. Corporate default rates remain low, but credit fundamentals are worsening. Non-financial issuers’ debt leverage ratios have increased due to weaker corporate earnings. Furthermore, higher interest rates have led interest coverage—the measure of how many times a company’s earnings can pay interest costs—to also worsen.

Nevertheless, we see pockets of opportunity in non-cyclical issuers, as well as opportunities in senior-ranking bank bonds. We remain cautious and favour higher quality, short-duration investment-grade bonds over high-yield bonds as the balance of risks is tilted to the downside.

A barbell approach presents the most attractive opportunities, in our view, as we would balance risks in corporate credit with higher-quality allocations in government bonds.

![[uns] house of commons, parliament](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/788182-featured-300x200.webp)