In the first quarter of the year, equity markets took the gold medal for resilience. By Fabiana Fedeli, Chief Investment Officer, Equities, Multi Asset and Sustainability, M&G Investments

Macroeconomic predictions are extremely difficult to ace at present. The direction of data (declining inflation and slowing demand) may be relatively easy to infer, but the timing, pace and extent of the moves, and whether these will occur in a straight line or (more likely) two steps forward and one, maybe two, backwards, is far more difficult to pinpoint.

The collapse, within quick succession, of Silicon Valley Bank (SVB), Silvergate, Signature and Credit Suisse is most likely going to become the subject of infinite business school case studies. We all thought that a credit crisis a la 2008, with a series of connected credit events, was a clear risk in the future. That said, it was relegated to the tails of the risk distribution curve and considered as the most extreme and feared recession scenario, which would – yet again – undermine trust in the financial system for a protracted period of time. But the bank failures that we witnessed in March were not the start of a systemic credit event (or at least it does not appear to be the case as of now), but rather the product of idiosyncratic issues. These incidents were quickly ring-fenced by regulators and central banks, with limited impact on the collective trust in the broader global financial system. Although concerns around regional US banks and smaller financial institutions are likely to persist.

In all of this, equity markets – which looked less attractive than their fixed income equivalents earlier this year, after a glorious January, a torrid February (and first half of March), and a decisive recoup in late March – took the gold medal for resilience.

What does this mean for what lies ahead

The market remains data driven and volatile, exacerbated by the increased volumes of short-dated derivatives. Behind all that noise though there are, ultimately, two key drivers that matter for markets: i) forthcoming central bank decisions (and any datapoints that can support the direction of travel in either direction), and ii) the likelihood, timing and depth of a recession. However, on both counts, while we can guess the direction of travel, the timing and intermediate steps are far from certain.

Central bank tightening should be close to the end, but we are still uncertain on when that end will come. The market still expects the Fed to cut from the second half of the year, which has continued to support equity markets. I fail to see the likelihood of rate cuts happening this year. If I am wrong, and cuts were to occur, it would spell bad news for risk assets – starting with equities – as they would most likely be triggered by a meaningful recession, which is not our base case scenario. The other trigger for a cut, inflation declining to ca. 2% later this year, appears even more unlikely.

And when it comes to the other key market driver; the likelihood, timing and depth of a recession, we are even more in the dark – or, at most, we only have a glimmering speck of light. Over the past month, we have seen a number of activity-related datapoints, globally, either remain weak or deteriorate, and there is a high likelihood that we will be facing further deterioration in demand. However, the timing and the extent of a recession remains uncertain at this point.

Let’s not forget that recessions can come with a lag. Looking at US data of recessions that appear triggered by a rate hike cycle from 1965 to date, recessions appear to occur to varying degrees and can appear with a wide range of lags of between five and 15 months from the last rate hike. Some recessions, like in the 1970s, started before the Fed ended its tightening, but the extent of hikes in the 1970s were much higher (960 bps and 1300 bps respectively in each successive recession period) than the expected terminal rates for this hiking cycle. Possibly the 540 bps of rate hikes between July 1967 and August 1969 were the closest to current times, headline inflation rose to 6% and the recession only started in January 1970 with a mild (-0.6%) GDP contraction. But, while history may rhyme, it doesn’t necessarily repeat itself. Market performance, and particularly the relative performance of equities versus fixed income markets, will hinge on the length and depth of a slowdown versus current expectations.

We maintain our stance that this is not a market for ‘broad strokes investing’ (taking directional macroeconomic calls and swinging entire portfolios one way or the other).

The market remains one where selection is the main driver of alpha, diversification is key and volatility has to necessarily become our friend

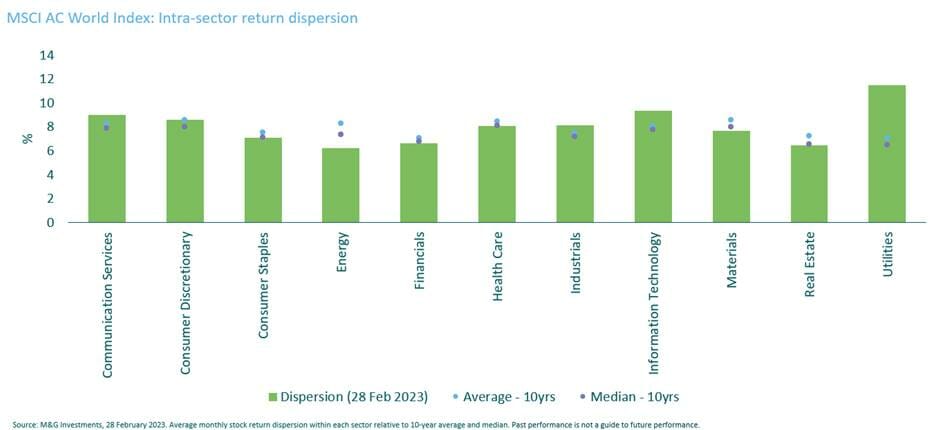

We remain focused on bottom up, differentiated research, rather than aspire to answer big macroeconomic questions. The market looks to be rewarding such an approach. The figure below shows how the dispersion of returns of stocks in the MSCI AC World Index have been trending above their 10-year average and median.

This is not only true between sectors, but, as shown in the figure below, in a number of cases also within sectors – where the dispersion of returns between stocks in a number of sectors is trending above the 10-year average and median, meaning that investors are making a distinction between companies with weaker and stronger prospects.

In our opinion, while at a broad index level equity and fixed income valuations appear to be accurately reflecting the set of risks and opportunities presented by the current macroeconomic backdrop, the pockets of mispricing are occurring at a more granular level. Think of the share price drop in financials around the world in March. The safer and more risky were victims of the same fate, offering a good opportunity for active managers to shop for investments in some high-quality financial institutions.

How are we preparing our portfolios?

In line with our belief in maintaining diversified portfolios, where selection is the key alpha driver and we stand ready to take advantage of tactical opportunities, our multi asset portfolios continue to hover around a neutral stance between equities and fixed income, and trade tactically around those positions, putting more focus on the underlying composition of the portfolios. More recently, we have taken some profit from equities, moving to a small underweight.

Within equities, we maintain our relative preference for non-US markets, where we find more compelling opportunities from a valuations vis-à-vis earnings profile standpoint. In fixed income, our multi asset strategies have moved to a neutral duration position from a small overweight. We did so by scaling back on the long end of the Treasuries curve after the recent rally. We also continue to like selected emerging market sovereigns and currencies, such as Brazil and Mexico. Elsewhere, we have been taking advantage of some opportunities in terms of both spread and outright duration exposure in areas of European Investment Grade credit across our Sustainable and Income strategies.

Across many of our portfolios, we maintain higher-than-average levels of cash to take advantage of tactical opportunities

Within equities, we have sold out of some more defensive names that had performed well in recent weeks. We took advantage of the market volatility to buy into higher-quality cyclicals, including large banks. These have strong credit and liquidity profiles, are tightly regulated, and yet saw a significant price drop amid recent events in the US and Switzerland.

From a country standpoint, we continue to find compelling opportunities in Japan, where a new datapoint is providing a further catalyst. Japan has been one of our favourite markets, as we have found a number of companies that are improving operational leverage with a positive impact on earnings growth, alongside increasing shareholder returns via raising dividends and share buybacks, even without the support of the macroeconomic backdrop. However, there may indeed be an emerging macroeconomic tailwind. Japan’s unions recently secured significant increases in this year’s shunto pay-bargaining round; the mean increase appears to be in the region of 4%, above market expectations and driven by labour shortages. According to our Japan investment team, this could be the trigger for the domestic economy to start experiencing some self-sustaining growth in the years ahead, as consumption responds to higher wages. Importantly, we believe that corporate profit margins will be able to offset the negative impact of higher wage costs given the gains in productivity that we have already started to see in the corporate sector and some transfer on pricing. This does not appear to be on the radar screen for most investors.

We have witnessed some unexpected events in the first quarter of 2023. Above all, the resilience of markets, particularly equities, has surprised many. Such resilience could persist in the months ahead, albeit not without bouts of volatility. We are, however, not out of the woods yet, and a number of risks could materialise and spoil the party: higher inflation (helped by the recent OPEC+ output cuts), an earlier-than-expected and deeper-than-expected slowdown in demand, and further woes in the financial sector. In the age of 24/7 mobile banking (which in the last quarter allowed c. 25% of deposits to take flight at two institutions within a day), a breakdown of trust in the financial system and a ‘run on’ deposits could bring down even the strongest bank. Anything is possible but offering clear predictions at this point is a futile exercise. In our opinion, a far smarter choice is to prepare.

![[UNS] celebrate](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/801986-featured-300x200.webp)