At the end of 2023, the UK’s FCA unveiled its Sustainability Disclosure Requirements (SDR) and investment labels regime for investment products, which includes a substantial package of measures aimed at improving the transparency of sustainable investment products and minimizing greenwashing.

These measures include four consumer-focused sustainability labels that asset managers will be allowed to use from July 31, 2024. The labels are “Sustainability Focus,” “Sustainability Improvers,” “Sustainability Impact,” and “Sustainability Mixed Goals.” All these are explored in new research from Morningstar.

New research available from Morningstar

Morningstar’s latest research “UK SDR Through the Looking Glass” explores the four labels and why they’re important. It also provides early insights into what the landscape of UK sustainability-labelled funds may look like by the end of the year. Their analysis is based on conversations with a selection of assets managers and their data and knowledge of the UK fund market. They also discuss the pros and cons of using labels as asset managers need to decide before December 2024. Finally, they attempt to answer a number of questions that asset managers and other market participants have raised in recent weeks.

Key takeaways from the report

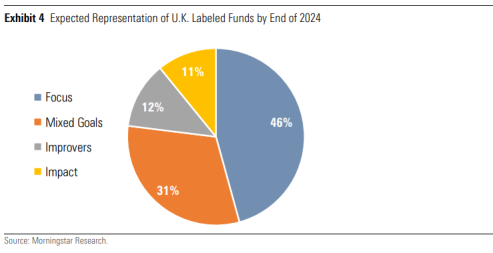

In their analysis, Morningstar have identified a number of important areas. They estimate that about 300 UK open- and closed-end funds will opt for a label by year-end, in what they call “an optimistic scenario”. Labelled funds may represent 8% of funds domiciled in the U.K. and less than 3% of all funds available for sale in the U.K.

They believe that “Sustainability Focus” will likely be the dominant label, followed by “Sustainability Mixed Goals”, then “Sustainability Improvers”, and “Sustainability Impact”.

In terms of the nature of the individual funds, equity funds may represent over half of the labelled product universe, according to Morningstar, while they anticipate that fixed-income and passive funds will be significantly underrepresented (each accounting for less than 10% of labelled products). There should be more options in the labelled allocation funds space by virtue of the introduction of the “Mixed Goals” label.

The report identifies reasons for using labels include investor demand, competitive pressure, and the benefit of clarity, among others. But some managers will consider the requirements too constraining. Some will take a cautious approach and wait and see how the market of U.K. labelled products develops.

Of course, the report reminds us that it’s likely that funds with similar aims could elect different labels, highlighting that labels can only be one indicator for investors, to be analysed in conjunction with other fund data and information.

SDR has already influenced the European Commission as evidenced by the proposed sustainable product categories in its recent SFDR consultation paper.

“The success of the UK labelling regime will lie in the quantity and quality of the products that get labelled. We expect conversations in the next few months and the first wave of implementation later this year to determine how this market will shape up.” Hortense Bioy, Global Director of Sustainability Research, Morningstar said. “We hope this early analysis will contribute positively to these conversations for the benefit of investors not only in the UK but also other jurisdictions as they look to implement similar regulatory frameworks”.