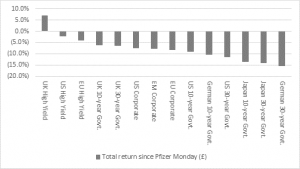

“Under such circumstances the record-low, even negative, yields available on bonds on offer a year ago look far less attractive and investors have taken evasive action. The longest-dated bonds have taken the biggest hit, which makes sense as their return profiles are so much more back-end loaded and farther away in the future. This is all explained by the concept of ‘duration’:

- Macaulay duration measures the average weighted time to maturity of all coupon and principal payments

- Modified duration quantifies interest rate risk and how much a bond or portfolio of bonds will move in price relative to a 1% shift in borrowing costs.

Source: Refinitiv data

“There is no guarantee that the trends of the last 12 months will continue. It is still possible to argue that inflation, deflation or stagflation could result from the current remarkable confluence of events, with Governments and central banks’ stimulative policies, vaccinations and an end to lockdowns boosting demand on one hand, and geopolitics, Government policies such as tariffs, and dislocations in the wake of the pandemic restricting supply on the other, with ever-growing debt piles sat in the middle.

“However, it seems clear that investors still have faith in central banks’ (and Governments’) faith to navigate us through this difficult period and maintain the status quo of loose, supportive policy, modest inflation and respectable levels of economic growth.

“This can be seen in two ways.

“First, the outperformance of equities relative to commodities over the past decade. Although ‘real’ assets have outperformed over past 12 months, they have not come close to making a dent in equities’ predominance. If inflation (or stagflation) do take hold, then that is not what markets are expecting or pricing in, so commodities, under that scenario could have a lot further to run.

Source: Refinitiv data

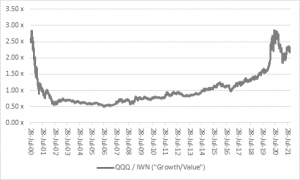

“Second, the clear outperformance of growth against value over the past decade. This makes sense in that inflation and interest rates have been low and growth hard to come by. Any company or industry capable of generating consistent earnings increases in that scenario was always going to be highly prized, and so it has proved with tech and social media and biotech stocks in particular.

“But if we get an inflationary recovery, then investors have no need to pay high valuations for jam tomorrow when they can pay much lower valuations for cyclicals and earnings growth (or jam) today, after those stocks’ underperformance of the past decade.

“The multi-trillion market caps of Facebook, Alphabet, Amazon, Apple and Microsoft continue to grab the headlines, but less highly-valued cyclicals are starting to rise more quickly, as can be seen in the last 18 months’ outperformance of the iShares Russell 2000 Value Index Exchange-Traded Fund (ticker IWN:NYSE) against the technology-and-growth laden Invesco QQQ Trust (ticker QQQ:NYSE).

Source: Refinitiv data

“If inflation really takes hold, and cyclicals and value and jam today stocks take over market leadership from long-term growth and tech and jam tomorrow stocks, there could yet be a violent change in how portfolios perform. Those investors with long memory will recall the stunning switch from growth to value that followed the peak in tech stocks in 2000 and how it took growth nearly two decades to reach the prior highs in terms of its relative performance relative to cyclicals and value.”

![[uns] house of commons, parliament](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/788182-featured-300x200.webp)