Despite the recent resilience of UK equities to tightening economic conditions, valuations across the asset class remain depressed as the market prices in a recession risk and longer-term inflationary drivers.

The UK market remains cheap compared with developed international markets, which provides a compelling investment opportunity on a 3- to 5-year view.

Alex Wright, Portfolio Manager of Fidelity Special Situations Fund and Fidelity Special Values PLC, believes there are plenty of reasons to be optimistic about the outlook for UK equities. Against a compelling valuation backdrop, he outlines why the UK remains a fertile hunting-ground for active stock pickers and highlights the unloved areas he is backing to deliver returns:

“After a sustained period of underperformance, UK markets started to see a turnaround from early 2021. Notably, the UK was one of the better performing markets in 2022, outperforming the US for the first time in six years.

“Despite this, general sentiment around UK equities has remained challenged. However, I am excited about the opportunity on offer today, where the current market is creating a fertile environment for active stock pickers to buy good, quality companies at cheap valuations.

Compelling valuations

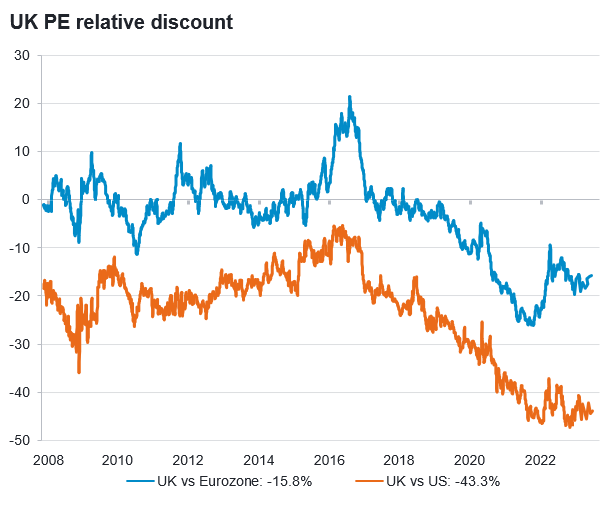

“Some have attributed the recent outperformance of UK equities to the composition of the index, which includes big value sectors such as energy and banks. But even adjusting for these sectors, the UK market looks cheap. Indeed, when we compare UK companies to their US counterparts, companies in the UK are significantly cheaper on a like-for-like basis.

Source: Peel Hunt, Refinitiv Datastream, 31 May 2023. For illustrative purposes only

MSCI Indices, 12m forward PE, IBES consensus,

“Interestingly, while the large-cap part of the market has outperformed due to strong earnings, the price to earnings ratio of all parts of the market is trading at roughly similar levels (around 10-11x earnings). This is leading to opportunities across the market cap spectrum.

Source: Fidelity International, Refinitiv DataStream, 31 May 2023. Data for FTSE 250 and FTSE Small Cap not available pre-1998

Value rally still has legs

“Over the past decade, we have experienced a prolonged period of very subdued inflation, low interest rates and modest economic growth. This has very much favoured growth companies at the expense of the unloved areas with lower downside risk that we favour.

“This trend began to reverse towards the end of 2020. Given the recent strong rally of value over growth stocks in the UK, investors may question if this can be sustained. In this regard, we would highlight that the current market environment of higher and stickier inflation, rising interest rates and economic volatility is more representative of the longer-term pattern seen over the last 100 years.

“History suggests that over the long term, value tends to outperform, given generally higher discount rates and a reversion to the mean. I therefore believe we are in the very early stages of a long-term rally in value stocks.

Focus on financials

“Some of the GDP sensitive stocks that did particularly well through the Covid recovery in late 2020/2021 are now looking less attractive. As a result, we have been selling some of these positions and we are slightly underweight this area, preferring to hold financials, with banks the second largest sector exposure.

“Banks have been unloved for a long period of time and investors have stayed away from the sector as falling rates and stronger balance sheet requirements have depressed earnings. Now however, tighter regulations have ensured better capital positions and strong funding resulting in higher levels of buybacks and greater profit sharing with shareholders now that fines have been paid off.

“There has also been a general misunderstanding of how interest rates influence earnings at banks. We have already seen a dramatic change in the earnings’ profile of interest rate sensitive banks like AIB and Natwest, resulting in a significant outperformance of these stocks.

“Aside from financials, we have more defensive positions in companies such as Roche, Imperial and Serco. We also own DCC and Mitie, which have some defensive as well as cyclical businesses. As such, the portfolio is diversified across sectors, but also, between defensive and more cyclical businesses.

“In terms of big sector underweights, the key one that stands out is consumer staples, namely due to valuations. Big international companies like Diageo or Unilever are good companies, but they are priced as such and therefore offer relatively low return prospects. The other area that I’m really avoiding is mining, where there is potential for earnings to fall meaningfully, with the outlook for the likes of iron ore and thermal coal particularly uninspiring.

Outlook

“While the economic environment remains uncertain, the relative attractiveness of UK valuations versus other markets and the divergence in performance between different parts of the market continues to create good opportunities for attractive returns from UK stocks on a three-to-five-year view. Within the portfolio, we are confident that our holdings, which have significantly lower levels of debt, possess the resilience to navigate a tough macro environment.”