Emma Maslin, financial coach said: “Every life opportunity we face is filtered through the lens of our unique money personality – or ‘financial tribe’ – but we often assume that others think about money in the same way that we do. Add to this a lack of communication between generations and there is a lot of room for misunderstanding and potential surprises later down the line.

“By taking the time to really understand our individual and respective family members’ ‘financial tribes’ we can leverage the positives of our different money personas to benefit ourselves and the overall family unit when planning for the future.”

Risks are short term as well as long

A lack of communication between parents and their grown-up children could have an immediate impact, given two thirds (65%) of parents plan on making meaningful wealth transfers in instalments over several years rather than in one lump sum when they die.

This approach could make a significant difference to a young adult’s short-term financial decisions, such as whether they should save for a deposit on a house or invest their money for the future. Yet only a quarter (28%) are aware of their parents’ plans and are therefore having to plan their futures without full information.

When one child gets a bigger inheritance – financial favouritism or pragmatism?

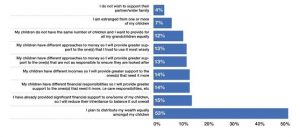

The main reasons given by the 47% of parents who do not plan to distribute their wealth equally among their children include a wish to even up previous financial support provided (15%), or because they felt certain children had different financial responsibilities and therefore a greater need for support (14%). Trust is another significant factor, with 13% of parents saying the child they trust with money will get more.

Chart 1. Reasons why parents plan to distribute different amounts of money to their children

Family ‘financial tribes’ further complicate wealth transfer

The study also explored the impact different ‘financial tribes’ can have on these significant decisions within families. According to the findings, parents who identified as Lifestyle Lovers or Big Spenders** were less likely to split their wealth equally among their children (4% and 17%), instead preferring to provide greater support to those that were not as confident with money to ensure they were taken care of.

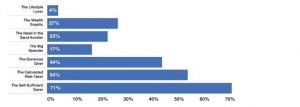

At the other end of the spectrum, those identifying as Self-Sufficient Savers were the most likely to split their wealth straight down the middle (71%).

Chart 2. Percentage of parents who plan to distribute their wealth equally amongst their children, by which financial tribe the parents identify with