In its latest monthly insight into the state of the UK housing market, Halifax has reported that property prices remain under pressure.

Sharing her summary of these latest property market data, Amanda Bryden, Head of Mortgages, Halifax, said:

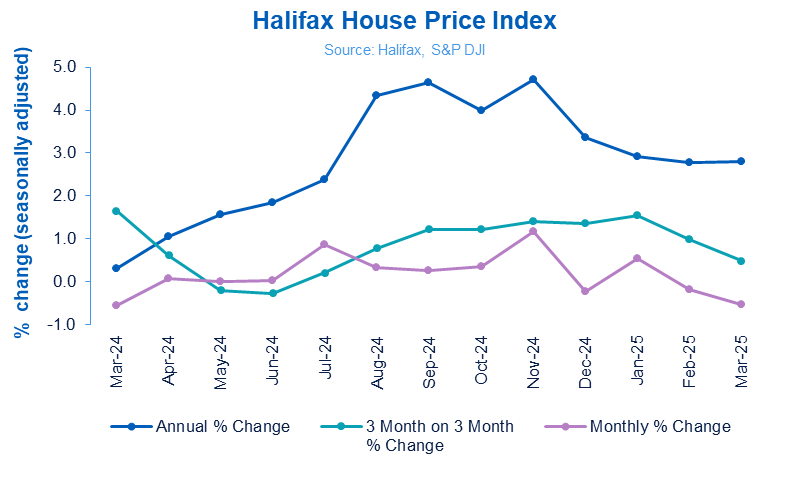

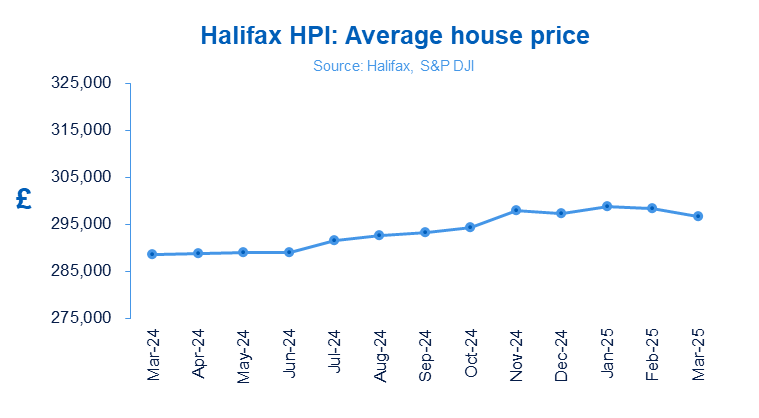

“UK house prices fell by -0.5% in March, a drop of £1,575. Despite this, the annual growth rate remained steady at +2.8%, with the typical UK property now valued at £296,699.

“House prices rose in January as buyers rushed to beat the March stamp duty deadline. However, with those deals now completing, demand is returning to normal and new applications slowing. Our customers completed more house sales in March than in January and February combined, including the busiest single day on record. Following this burst of activity, house prices, which remain near record highs, unsurprisingly fell back last month.

“Looking ahead, potential buyers still face challenges from the new normal of higher borrowing costs, a limited supply of available properties to choose from, and an uncertain economic outlook.

“However, with further base rate cuts anticipated alongside positive wage growth, mortgage affordability should continue to improve gradually, and therefore we still expect a modest rise in house prices this year.”

Nations and regions house prices

Northern Ireland continues to record the strongest annual property price growth of any nation or region, rising by +6.6% in March. House prices average £206,620.

Scotland recorded the second strongest house price growth, increasing to +4.3% last month, compared to +3.8% in February. The average house price is now £213,750.

Property prices in Wales were also up +3.7% in March to an average of £227,332.

In England, Yorkshire and Humberside also saw strong growth, up +4.2% year on year, with properties now costing an average £215,807.

London saw the slowest annual house price growth, from +1.5% in February to +1.1% in March. The capital remains the top spot for the highest average house price in the UK, at £543,370.

Commenting on these latest data, Jonathan Handford, Managing Director at national estate agent group Fine & Country, said: “House prices dipped in March, reflecting a market adjusting to economic shifts and tax policy changes.

“As the April deadline for stamp duty changes loomed, many buyers rushed to complete purchases to avoid higher taxes, but the timing caused a softening of prices month-on month.

“With the stamp duty relief threshold for first-time buyers dropping from £425,000 to £300,000, March marked the closing of a key window of opportunity — sparking what some dubbed the ‘awful April’ rush, as buyers scrambled to avoid higher stamp duty costs.

“Adding to the cautious sentiment, inflation unexpectedly dropped to 2.8%, offering a glimmer of hope that cost-of-living pressures may ease.

“Although the Bank of England held interest rates at 4.5% in March, some experts are now anticipating the possibility of further rate cuts due to falling inflation and global economic challenges, such as new US trade tariffs. This could see lenders start offering slightly lower fixed-rate mortgage deals.

“For first-time buyers, the combination of falling inflation, more stable borrowing conditions, and the urgency around tax changes created a brief window of opportunity. However, affordability remains a challenge, particularly in higher-priced areas, and the rise in the stamp duty threshold will only make it more difficult.

“While March saw a dip in house prices, demand may temper post-deadline. However, with spring being a traditionally busier period for sales, there’s potential for activity to pick up, particularly if expectations for interest rate cuts continue to grow.”

Nathan Emerson, CEO of Propertymark comments: “This house price reduction will be a huge disappointment to many sellers hoping to make gains on a house sale to climb up the housing ladder, but it could also be an opportunity for aspiring homeowners to take advantage of the slight reduction in house prices and take their first step, or next step, onto the housing ladder.

“Hopefully this month on month dip is only temporary. The spring and summer months normally spur on a flurry in housing activity, especially at a time when there are many competitive mortgage deals out there right now as a result of the reduction in interest rates last year.

“However, with housing playing a vital role in the UK economy, international events could jeopardise the Bank of England’s target of a 2 per cent inflation rate, which may thwart their ambitions to reduce interest rates further. The housing market must remain stable ahead of the Bank of England’s next decision on interest rates in May.”

Mark Eaton, Chief Operating Officer at April Mortgages, comments: “A dip in house prices was always likely, following the surge in activity earlier this year, as buyers rushed to complete before the stamp duty holiday ended. With that incentive now gone, sellers may need to show more flexibility on their asking price to secure a sale.

“The next few months will be a litmus test for the property market. With no new support measures in place and households facing rising costs on essentials like energy, water, and council tax, many buyers are understandably taking a more cautious approach – and that’s already feeding into slower activity levels.

“The Government has pledged to make housebuilding one of its top priorities over the coming years. The shortage of stock in many parts of the country is what is keeping prices high.

“The affordability factor is key to getting more first-time buyers on the property ladder and ensuring that the market does not see a considerable readjustment in prices this year. If inflation was to keep coming down and interest rates followed suit, it would provide some relief.

“While there isn’t a silver bullet for the issue, longer-term modern fixed rates which provide access to larger loan amounts may become a lifeline for those struggling to save for a deposit.”