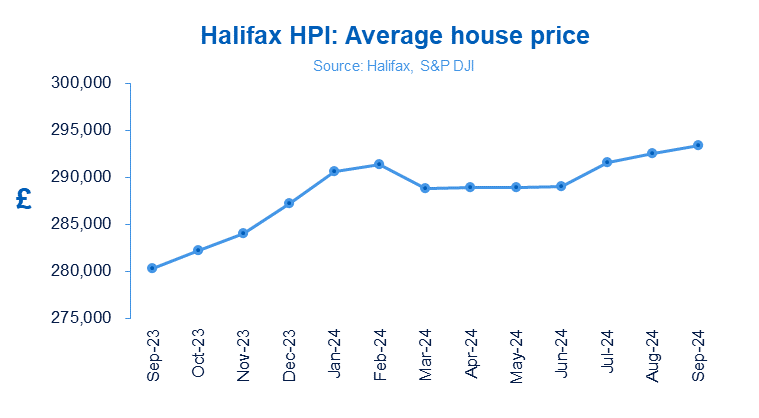

Halifax have released their House Price Index, which has revealed that house prices have risen for a third successive month. House prices increased by +0.3% in September, matching the rise seen in August.

The Year-on-year prices are up +4.7%, which is still the strongest rate since November 2022. Higher annual growth reflects the base impact of weaker prices a year ago. Typically, property now costs £293,399 (compared to £292,540 in August), the highest since June 2022, while the average amount paid by first-time buyers is now around £1,000 less than two years ago. Northern Ireland continues to record the strongest annual house price growth in the UK.

Amanda Bryden, Head of Mortgages, Halifax, said:

“UK house prices climbed for the third month in a row in September, with a slight increase of +0.3%, or £859 in cash terms. Annual growth edged up to +4.7%, the highest rate since November 2022. This brings the average property price up to £293,399, just shy of the record high of £293,507 set in June 2022.

“It’s essential to view these recent gains in context. While the typical property value has risen by around £13,000 over the past year, this increase is largely a recovery of the ground lost over the previous 12 months. Looking back two years, prices have increased by just +0.4% (£1,202).

“While improved mortgage affordability should continue to support buyer activity – boosted by anticipated further cuts to interest rates – housing costs remain a challenge for many. As a result we expect property price growth over the rest of this year and into next to remain modest.”

Nations and regions house prices

Northern Ireland continues to record the strongest property price growth of any nation or region in the UK, rising by +9.7% on an annual basis in September. The average price of a property in Northern Ireland is now £203,593.

House prices in Wales also recorded strong growth, up +4.4%, compared to the previous year, with properties now costing an average of £224,119.

Scotland saw a more modest rise in house prices, where a typical property now costs £205,718, +2.1% more than the year before.

The North West once again recorded the strongest house price growth of any region in England, up by +5.1% over the last year, to sit at £234,355.

London continues to have the most expensive property prices in the UK, now averaging £539,238, up +2.6% compared to last year. This is still some way below the capital’s peak property price of £552,592 set in August 2022.

Commenting on today’s data, Nicky Stevenson, Managing Director at national estate agent group Fine & Country, said:

“UK house prices continued to edge higher in September — the strongest rate since November 2022 — signalling the start of the typical autumn market boost.

“Though the Bank of England held interest rates steady at its most recent meeting, it signalled that borrowing costs are gradually on the path down from their highest levels since the 2008 financial crisis. And another cut is still being predicted towards the end of this year.

“In response, lenders such as Nationwide, Halifax, and HSBC have lowered five-year fixed mortgage rates to below 4%. This easing of mortgage rates, along with banks increasing their lending capacity, is giving buyers renewed confidence.

“While this is positive news for homeowners, affordability challenges persist for many potential buyers still adjusting to historically higher mortgage costs.

“Despite recent signs of market stabilisation, elevated mortgage rates continue to lock many prospective buyers out of the market. While the average amount paid by first-time buyers is now around £1,000 less than two years ago, this demographic remains sensitive to borrowing costs.

“With market activity picking up and the possibility of further rate reductions, modest house price growth is expected to continue through the rest of 2024. However, this growth may be uneven, with regional variations based on local demand and economic conditions.”

Tom Brown, Managing Director, Real Estate at Ingenious, said: “Today’s data shows that the resilience and appeal of the UK property sector persist. Though we have seen higher inflation and sticky borrowing rates, we welcome the BoE’s focus on rate cutting and what will hopefully be the start of the much needed falling rate cycle.

“There’s clearly a significant and notable shortage of housing inventory across various price brackets and locations. Consequently, any decline in homeowner sales is likely counterbalanced by increased demand from renters and investors. This is a trend that is not going away. However, it’s crucial to recognise that the situation isn’t consistent nationwide or across different property pricing brackets. It’s helpful to delve into subsectors and regional dynamics when assessing opportunities, as a broad market view can be misleading. In the real estate sector, we’re seeing significant investment capital for assets for long-term rental. On account of their scale and buying power, these typically institutional investors face fewer disruptions than owner occupiers or small-scale Buy-to-let investors.

“At Ingenious, we continue to work closely with borrowers and investors, adapting to the dynamic market landscape and broader economic shifts, including those related to the climate crisis and changing lifestyles. We are expanding the reach of our development lending product to provide extended stabilisation terms for specialised developers in the rental sector. Furthermore, we’re introducing special lending terms for developers focused on reducing embedded carbon in their construction practices.”

Daniel Austin, CEO and co-founder at ASK Partners, said: “We are continuing to see a consistent month-on-month rise in house prices, which signals a potential upward trend for the remainder of the year. The market is showing strong signs of resilience, even amid broader uncertainties. Much anticipation surrounds Labour’s plans to stimulate the housing sector, particularly regarding the construction of new homes and unlocking the planning system. If effective initiatives are announced in the coming months, they could provide the market with an additional boost, driving further growth and confidence in the sector.

“In the property investment world, rent values have seen sustained growth, positioning real estate as reasonably valued in comparison to gilts and presenting growth potential. In the realm of commercial real estate, we have seen values hit the bottom and confidence return. The market has picked up with opportunistic acquisitions of prime properties in prime locations.

“As a debt provider, we hope to support well-capitalised borrowers who understand their product and are looking at the best sites in prime locations with potential to add to their asset value. Following this strategy, we aim to bolster developers’ initiatives with the flexible underwriting approach that is necessary for navigating a changing market. This will enable us to continue to offer opportunities for the growing number of private individuals opting to invest in property debt.”

Nathan Emerson CEO at Propertymark comments:

“It is very welcome news to see yet further growth in the housing market and taking a wide-angle view of the year, there is no doubt consumers are now able to approach the buying and selling process with a far greater degree of confidence compared to the very start of the year. There is still further progress to be made, but with strong hints we may see further dips in the base rate before the year is out, we are seeing some lenders already confident enough to switch up their mortgage offerings which is proving very welcome news for borrows.”

Also commenting on the data, Chris Little, Chief Revenue Officer at finova said: “Today’s data from Halifax confirms that the housing market is on steady footing, energised by falling borrowing costs and a surge in buyer interest. Across the market, the industry is optimistic and seems to be in agreement that growth is gathering momentum. With hopes that the Bank of England will gradually ease interest rates, borrowers could soon see more stable buying conditions. All eyes are now on the upcoming Autumn Budget, where the government may finally address ongoing affordability issues and limited housing supply – potentially bringing much-needed relief to buyers and sellers alike.

“In this current climate, lenders are locked in intense competition, with both high street banks and specialist lenders cutting rates to attract business before year-end. Speed-to-market is critical, and technology is the key to ensuring seamless property transactions for customers. Whether it’s adopting a cutting-edge pricing engine to swiftly adapt to market shifts or upgrading a new banking platform for self-service product changes, lenders need to invest in these innovations early to stay ahead and maintain their competitive edge.”

Mark Eaton, COO of lender April Mortgages, comments:

“The Halifax house price figures for September 2024 reveal a stable housing market, with a modest 0.3% increase in property values compared to the previous month.

“Typically, we’d expect the housing market to gain momentum after the summer holiday lull as both buyers and sellers become more active. This modest uptick indicates steady demand, supported by stabilising interest rates. However, affordability remains a challenge, particularly for first-time buyers still grappling with high living costs.

“Mortgage affordability remains key to sustaining a strong housing market. The expectation of further rate cuts, with another possible reduction in November, coupled with ongoing competition among lenders, may continue to drive mortgage rates down. This positive trend sets the stage for a potentially strong final quarter in the property market.

“All eyes are now on Rachel Reeves’ upcoming Budget on 30th October 2024, which could significantly impact the housing market. Increased government borrowing to address the £22 billion deficit might push interest rates higher, raising mortgage costs.

“On the flip side, measures such as support for first-time buyers, stamp duty reforms, or government-backed mortgage guarantees could help offset these challenges and maintain market activity.”