Judging by interest rate market pricing, this week’s BoE meeting should be one of the least interesting of the major central banks. Following the surprisingly split decision to ease in August, commentary on and from the BoE has drifted more hawkish (Figure 1). Interest rate markets now do not fully price another 25bps ease until next April.

The easing cycle that has so far delivered 125bps worth of cuts in a year is assumed to be on hold for now. Moves at the long-end of the UK curve, however, may yet produce market moving news from the September meeting, which brings with it the annual MPC judgement on the pace of quantitative tightening (QT).

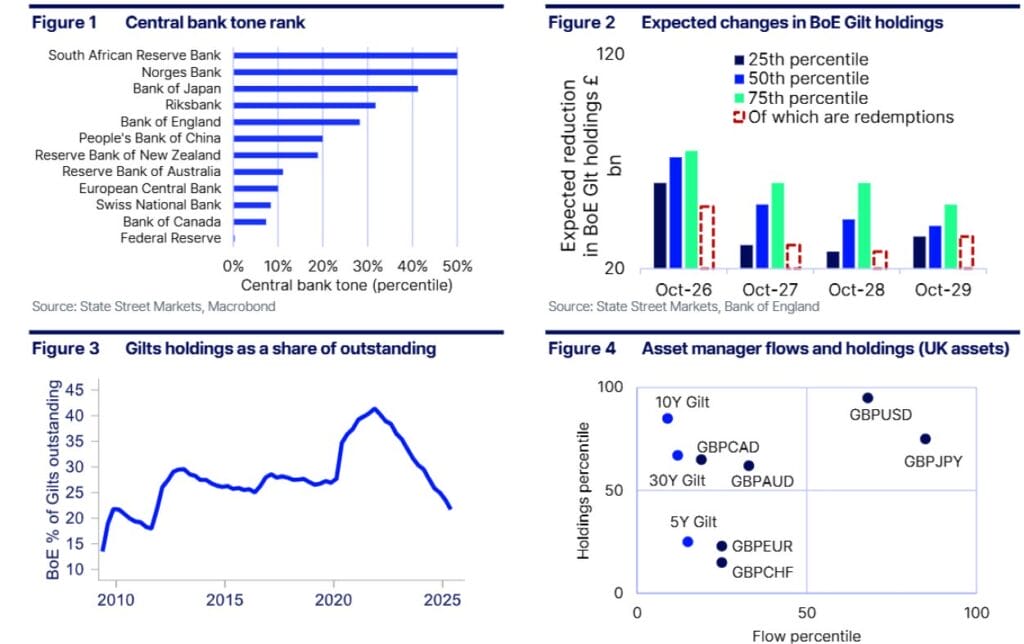

A year-ago the MPC voted to maintain the planned £100bn reduction in the stock of the bank’s Gilt holdings to £560bn. Most of this was passive (allowing Gilts to mature), similar to the approach of other major central banks. But there were also £13bn worth of active sales. The question for 2026 (or the year to October 2026 to be exact) gets a little harder, the BoE’s Gilt stock will only fall by £49bn from bonds maturing. According to the BoE’s survey of market participants (MAPS) the median expectation is for a stock reduction of £72bn this year(Figure 2), followed by a £50bn fall the year after – a gradual reduction in balance sheet size in keeping with central bank guidance that QT should be like watching paint dry.

However, while that might be true in normal times, sovereign bond markets have been anything but boring recently. While UK short-rates have fallen 125bps in the past year, longer yields are up more than a 100bps. The UK is not alone in this, but the BOE is the only major central bank engaged in active bond sales. Given as a share of Gilt issuance the BoE’s holdings are already down to 20% of the market (Figure 3), it is fair to question if such active sales are necessary. The combination of BoE APF redemptions and increased issuance will take this number down to 11% by 2029 without any sales.

Further, the bank’s estimate of the Preferred Minimum range of reserves has crept higher to £385- 540bn. Without any active sales the BoE would achieve this in the coming year. In short, there is a case for a more dramatic end to QT, even it if was simply to stop active sales and allow redemptions to do their work. This relatively less hawkish outcome would potentially challenge investors’ current GBP overweight positions against the USD and the JPY, but may help the investor unwinds currently underway in 10 and 30-year Gilts.

![[UNS] tax](https://ifamagazine.com/wp-content/uploads/2024/11/getty-images-gA9N92x8Yko-unsplash.webp)