The Alternative Investment Market has turned 21 and Richard Power, Head of Smaller Companies at Octopus Investments, looks at what makes it a success

Having recently celebrated its 21st birthday, the Alternative Investment Market (AIM) has faced more than its fair share of character-building events through the years.

Back in 2000, the junior growth market of the London Stock Exchange (LSE) survived the aftermath of the dotcom bubble, a turbulent period which hastened the demise of its French and German counterparts. AIM also successfully navigated its way through the global financial crisis. In fact, in 2008 and 2009, when other financing doors were being slammed shut, fast-growing AIM-quoted companies managed to raise £10 billion. The resilience of AIM was tested once again in 2010, as the commodity price bubble deflated, by which time 45% of AIM by value was exposed to companies in the resources sector. Therefore, neither Brexit nor the proposed merger between the LSE and Deutsche Boerse should hold any fear.

The secret behind the success of AIM is its ability to evolve. When it was launched in 1995, AIM was intended to be a platform for small growth companies to gain access to capital. In that respect, it has succeeded spectacularly, raising over £96 billion of funding on behalf of over 3,600 companies, supporting over 750,000 UK jobs. The indirect impact of AIM – for example benefits to suppliers and employees spending wages, shows total economic contribution of £25 billion of GDP, which is more than the UK’s aeronautical or pharmaceutical industries.

AIM: the facts and figures

- Since its inception in 1995, the market has supported more than 3,500 AIM companies.

- By the end of 2014, UK-incorporated AIM companies represented 81% of all new admissions to AIM and 80% of the total stock of AIM companies.

- AIM companies contributed £14.7 billion to UK GDP and directly supported more than 430,000 jobs in 2013. To put these numbers in context, the UK aerospace and automotive industries – two of the UK government’s key industrial sectors – make an economic contribution of £9.4 billion and £11.5 billion respectively, while the UK pharmaceutical sector contributes £13.3 billion.

- AIM companies made a significant tax contribution of £2.3 billion to the Exchequer

AIM is home to a wide variety of companies that offer the potential for growth and dividends. The market has had some tremendous success stories over the years. When online fashion retailer ASOS turned to AIM in 2001 as a very small loss making e-commerce business, options for growth capital were limited. The dotcom bubble had burst and confidence in online business models had been severely damaged. ASOS found the funds it needed via AIM and has since gone on to become a global success story, currently valued at over £3 billion. Today, AIM is thriving and attracting a range of UK success stories. Well-known British brands, including Fevertree Drinks, Joules and Hotel Chocolat, have all recently turned to AIM in order to fund the next stage of their growth.

Not all plain sailing

But while investors may choose to access AIM through direct investments, the necessary due diligence requires time, resources and experience. It’s in the nature of smaller companies that not all of them will survive. Therefore, investing via a dedicated AIM-focused fund is likely to alleviate some of these concerns, while potentially also increasing the diversification benefits to investors. Active management generates most value when an asset class is inefficiently priced. This is certainly the case with smaller companies where a lack of research and market coverage creates pricing inefficiencies, which are typically exacerbated following a period of volatility. Expertise and focus in smaller company AIM-listed shares therefore creates the opportunity for significant outperformance, and active management can bring the potential of AIM to life for investors.

Successive governments have acknowledged the importance of AIM as part of the UK’s growth capital eco-system, and a number of AIM stocks offer tax incentives designed to encourage those investors prepared to take on the higher risks associated with backing smaller companies. Tax incentives made available through EIS and VCTs have played an important role in maintaining investor appetite across the full market cap spectrum on AIM. Alongside these is another valuable incentive called business property relief (BPR). Shares that qualify for BPR become exempt from inheritance tax after two years, provided the investor still holds the shares upon death. In addition, the government has abolished stamp duty on the purchase of AIM-quoted shares and further broadened the market’s appeal by allowing AIM-quoted shares to be held via an ISA. In short, there are many ways in which investors can capitalise on AIM stocks tax efficiently.

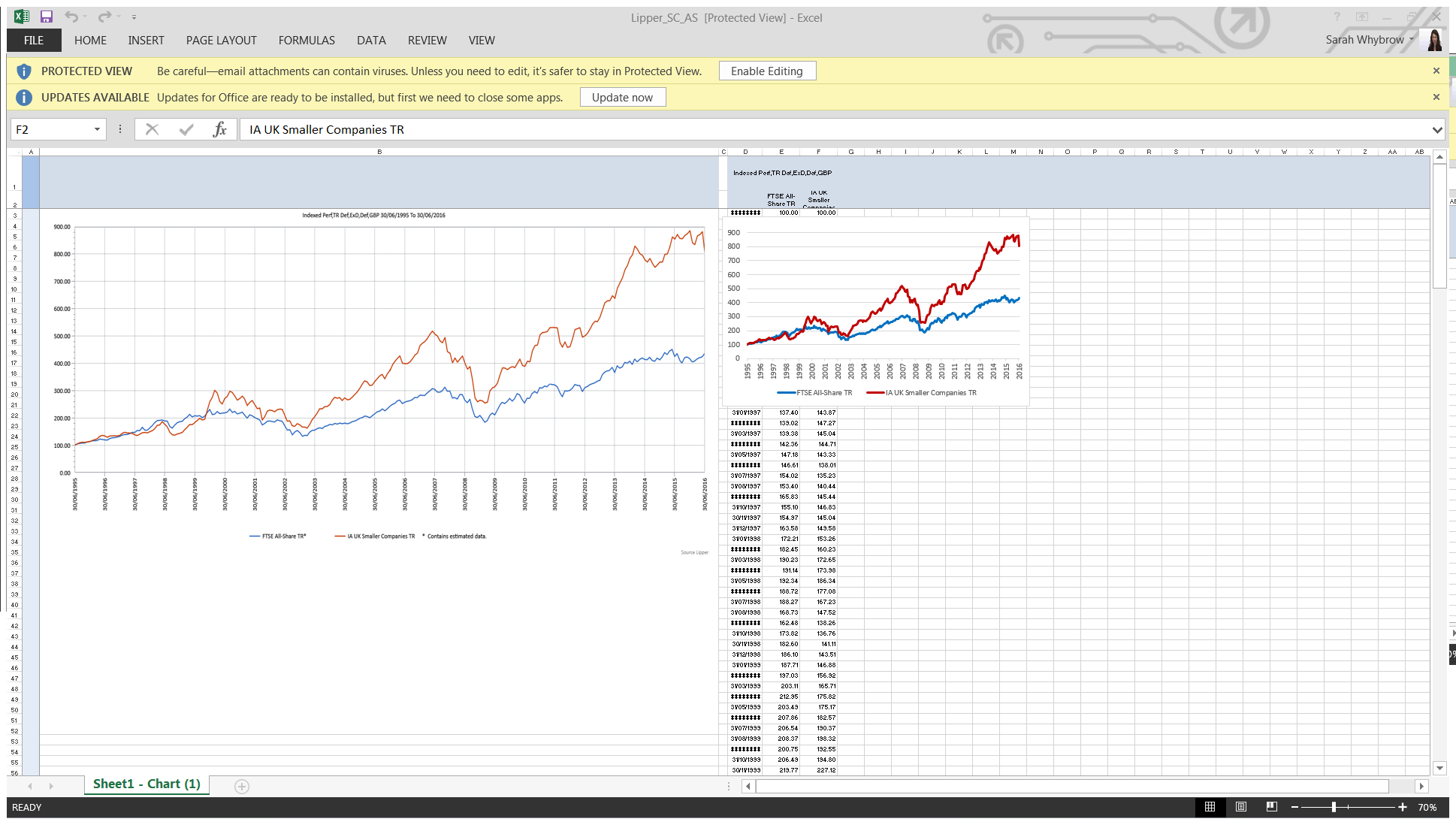

The best way for investors to approach smaller companies is to take a long-term outlook. As the chart below demonstrates, while the asset classes are not comparable on a like-for-like basis, smaller companies have outperformed larger companies considerably over longer time periods. There’s no real mystery here – smaller companies simply grow their earnings faster. Therefore, provided investors have a long-term horizon (of more than five years), and are willing to accept higher risks in pursuit of higher potential returns, actively managed AIM portfolios offers enormous investment potential.

Source: Lipper, 30 June 2016. Indexed Performance, Total Return from 30 June 1995 – 30 June 2016.

Over the years, AIM has succeeded by staying true to its founding principles: accessibility for ambitious growth companies, open to investors of every kind, a regulatory approach that recognises the needs and capacities of growth companies, and a market open to learning and evolution. Such positive attributes are needed now more than ever. In other countries, many of which have failed to establish a market for smaller companies, AIM is envied as a great source of long-term finance for innovative, aspirational companies requiring capital to reach their full potential. We don’t expect that to change any time soon.