Written by Paula Steele, director at John Hill Lamb Oldridge

Many clients are concerned that there may be changes to capital gains tax and Inheritance tax in the Budget on 30th October and they may well be right! In order to potentially avoid these potential tax changes many clients are making gifts in the hope that they will fall into the current tax regime.

The gift may well trigger capital gains tax – on residential property assets the tax will be at 28%, on non-residential property and all other assets it will be 20%. The tax on residential property gains has to be paid within 60 days from the date of completion, on all other assets by 31st January 2026. Clients should take advice with regard to how much tax will be payable as the gain is payable on the difference between the cost price, including further expenditure that has been made and the sale price of the asset and identifying the cost price can be challenging. Many clients feel that a 20% capital gains tax rate is unlikely to be maintained and are happy to trigger the tax now. It also enables portfolios to be restructured which can be helpful going forward.

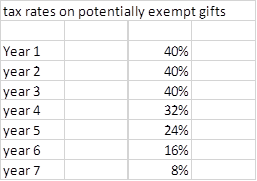

Once the CGT hurdle has been addressed then if it is a direct gift, or a gift into a bare trust it will rank as a potentially exempt gift with no immediate IHT payable. However if the donor dies within 7 years then the tax will trigger – at 40% on the value of the gift at outset for 3 years and then tapering over the following 4 years on the following basis:

If a client has not utilised their Nil Rate Band (NRB) for IHT, which currently stands at £325,000, then the gift will be allocated against this and on this element there will be no taper relief. The NRB will be utilised against any gift being made and will refresh after 7 years. As effectively the NRB is lost against the balance of the estate, many clients insure the tax on the first £325,000 of gift, with a sum assured of £130,000 on a 7 year, level basis.

If the gift is made to a discretionary trust then it will rank as a chargeable lifetime transfer, with a 20% initial tax rate, and the balance of the 40%, tapering, paid if the donor dies within 7 years. If gifts are made to a discretionary trust then capital gains tax can be held over which allows for the tax to be deferred until the asset is realised but with the donor’s initial base cost for calculating the tax.

It is possible to buy insurance to cover the potential liability – a few insurers offer a single contract which will pay out on the reducing term but most insurers offer a series of term insurances, running off as the liability reduces and with costs reducing as well .

We always aim to put the cost in context and show it as a percentage of the gift – the clients have to consider whether they wish to commit to a known, low cost for insurance or to leave a potential, much larger liability running.

If the clients don’t want to buy insurance they need to consider how the tax would be funded in the event of their death in the 7 years: Will the beneficiaries have spent the money? Perhaps by paying off mortgages, on school fees, on getting children onto the property ladder? Furthermore, while one beneficiary may retain the funds to pay the potential tax, another may not.

To give an idea of costs per £1,000,000 gift with an initial £400,000 liability:

| Age 30 | 40 | 50 | 60 | 70 | 80 | |

| Year 1 | £163 | £240 | £440 | £1,096 | £3,061 | £11,718 |

| Year 2 | £163 | £240 | £440 | £1,096 | £3,061 | £11,718 |

| Year 3 | £163 | £240 | £440 | £1,096 | £3,061 | £11,718 |

| Year 4 | £131 | £193 | £357 | £892 | £2,511 | £9,516 |

| Year 5 | £99 | £147 | £274 | £689 | £1,961 | £7,314 |

| Year 6 | £66 | £99 | £186 | £471 | £1,354 | £5,113 |

| Year 7 | £33 | £50 | £95 | £241 | £701 | £2,683 |

| Total Paid | £816 | £1,208 | £2,231 | £5,581 | £15,711 | £59,779 |

| Cost as a % of the gift | 0.08% | 0.12% | 0.22% | 0.56% | 1.57% | 5.98% |

![[UNS] celebrate](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/801986-featured-300x200.webp)