Short-term pain

Elevated energy costs, supply chain disruptions, and reduced demand as the uncertainty of the war dampens consumer spending will all conspire to dent the European economic recovery in 2022, in our opinion. Thankfully, this unwelcome turn comes after the region’s economy started the year on a relatively strong footing, benefiting from the lifting of COVID-19-induced restrictions.

Nevertheless, economic forecasts are being revised down. Lascelles recently further fine-tuned his 2022 projection for the eurozone’s GDP growth to 2.5 percent, down from 3.8 percent early this year. More adjustments are likely in light of the rapidly evolving situation.

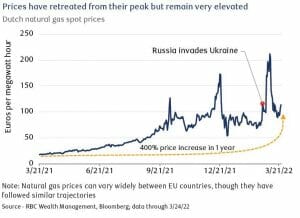

The recent decline in energy prices could give the region some respite and we are also watching for potential fiscal spending announcements, as such injections could lift growth. But the impact of the war on consumer and business sentiment, and whether energy-intensive companies have to cut output should there be further restrictions on Russian energy—be they imposed by the EU or Russia turning off the taps—could weigh further on economic activity.

Lascelles looks for inflation to peak higher this year as a result of the conflict, at around eight percent year over year. Worried about such a high level, and the impact of the war on economic growth, the European Central Bank (ECB) is angling for some flexibility. While it announced it will accelerate the reduction of its asset purchase programme, now aiming to end it in Q3, the ECB also suggested it could increase bond buying again if circumstances warranted. Furthermore, the ECB’s statement after the March 10 policy meeting omitted the comment that rates could rise shortly after the end of asset purchases. RBC Capital Markets expects the ECB won’t increase interest rates before 2023.

Stock market implications

In the medium term we expect fiscal spending should underpin growth, while over the long term the EU could eventually emerge from the conflict with stronger institutions. But the short-term outlook is nevertheless more complex than it was earlier this year.

The MSCI Europe ex UK Index is down more than 10 percent in local currency terms since its January high, leaving the index to trade at 14.3x the forward consensus earnings estimate, a steeper-than-average discount to the U.S. on a sector-neutral basis. This low level suggests that the reductions in growth forecasts largely appear to be factored into the current valuation.

Yet we think it is prudent to downgrade European equities to Market Weight from Overweight given it is a market with a relatively high proportion of cyclicals.

We still believe there is an attractive opportunity in stocks related to the green energy transition. This remains very much a priority for the EU, and, if anything, it is now seen as a security issue and not just an environmental matter. Europe continues to be a leader in this area and we think compelling opportunities can be found after the recent correction.