The hit to UK homebuyers’ confidence from the mortgage-market upheaval is likely to drag house prices in H2 as the pool of buyers shrinks, while some homeowners decide to sell – though Bloomberg Intelligence (BI) analysts believe it will be less marked than in the global financial crisis – as well as small landlords amid surging loan repayments, finds BI’s latest UK Housing Pulse.

UK housing activity had been slowly recovering in H1 as mortgage rates fell from their Q4 peak.

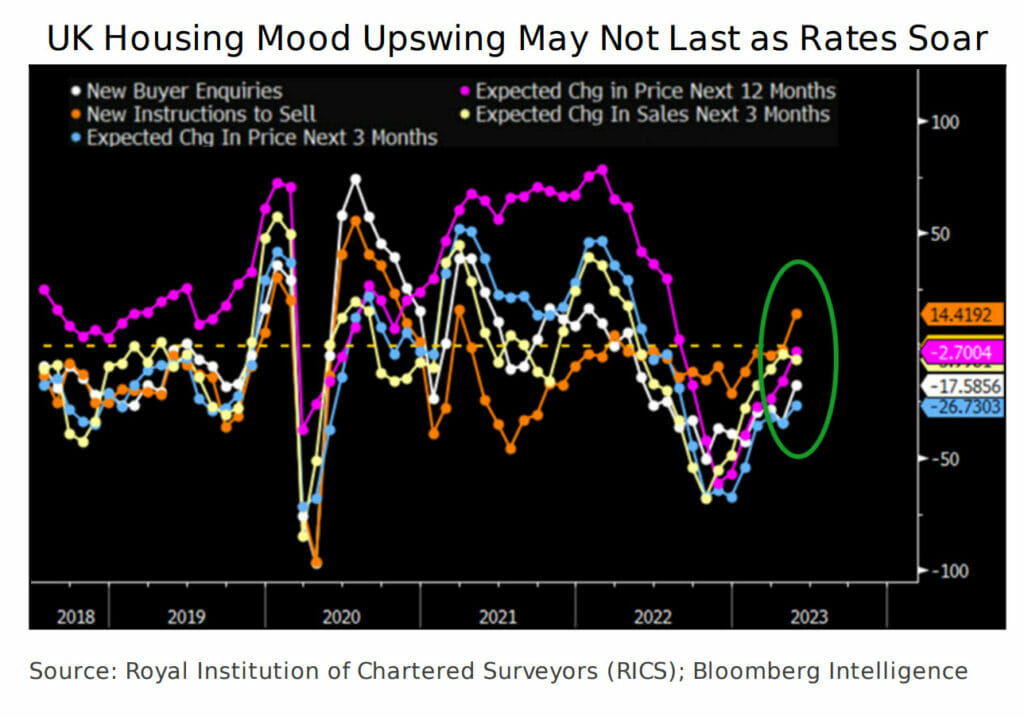

Iwona Hovenko, senior real estate analyst at Bloomberg Intelligence said: “Soaring mortgage rates – as peak Bank of England rate views surged by 100 bps in just one month due to persistent inflation – pose a renewed threat to UK housing activity and prices. The shift risks undoing the fragile progress made earlier this year from the lows of Q4, suggesting the woes of UK homebuilders Persimmon, Barratt, Taylor Wimpey, Bellway and Berkeley may last longer than we previously anticipated.”

In May, the Halifax house-price index fell 1% annually – for the first time since 2012 – yet this was driven by a base effect, as prices were unchanged vs. April compared to an increase in May 2022. The Nationwide index was also static sequentially in May, despite the 3.4% annual price decline, owing to a stronger performance a year earlier. The Rightmove house price index was flat in June after reaching a peak in May.

One Month Is a Very Long Time for UK Housing

Elevated interest-rate expectations could hit the UK housing market even before the Bank of England hikes rates, given they drive the steep increase in mortgage rates that poses a material risk to housing activity and prices. Much higher-than-forecast inflation and wage growth reported in May and June have fuelled bets for peak rates of 5.75% vs. about 4.8% just a month ago. This has been followed by a similar dramatic spike in swap rates, which then pushed up mortgage rates. Yet with BOE rate expectations very volatile, once inflation starts easing, those views could potentially moderate quickly, offering the UK housing market a respite, though this may require several months of consistently falling inflation – while latest data have shown it remains sticky – implying risks for housing may be tilted to the downside.

Fragile UK Housing Recovery at Risk From Soaring Rates

Hovenko, continues: “The recent sharp mortgage-rate hikes will hit UK housing sentiment, especially given the fragile rebound from post-mini-budget lows in Q4. While surging rates may add urgency for buyers who have already secured a more-attractive mortgage offer, other househunters may delay purchases until rates fall and housing-market headwinds ease. Soaring rates may create a spiral of panic among homeowners looking to remortgage before rates rise even more, which may fuel more hikes as lenders withdraw cheaper deals to curb applications. ”

BOE data for May doesn’t yet reflect the latest steep increases, though, anecdotally, price comparison websites flag the lowest five-year fixed rates on a 75% loan-to value (LTV) mortgage soaring by about 60 bps to 4.8% in a matter of days. Best-buy 60% LTV deals may have jumped even more to about 4.7%.

UK’s Mortgages Top £1.6 Trillion; Rates Could Exceed 5% in 2023

A revival in UK mortgage approvals appears set to slow or even plateau in H2 amid expectations of higher interest rates. The elimination of an affordability stress test – against a standard variable rate plus 3% – might only offer borrowers limited support. With mortgage rates poised to exceed 5% vs. above 6% in November for 75% loan to value, we expect the volume of monthly approvals to be about or below £20 billion vs. the £25 billion initially projected.

Tomasz Noetzel, banking analyst at Bloomberg Intelligence added: “Since 2021, several lenders (Halifax, HSBC) lifted the loan cap to 5.5x income. We believe significant softening is possible as the government lobbies banks for support for consumers most affected by the inflationary squeeze on income. Lenders may be more flexible with refinancing since mortgage holidays aren’t on the agenda.”

UK Mortgage Approvals Fall Below £11 Billion

Noetzel, continues: “An increase in remortgaging (more likely on five-year fixed terms) could partly offset the drop in first time-buyer volume as higher interest rates and a painful squeeze of households’ disposable income slowly alter banks’ mortgage-growth mix. April’s new-homebuyer mortgage approvals fell below £11 billion after recovering from January’s low level, and we don’t expect that trend to change significantly in the coming months, with some lenders pulling mortgage offers in response to rising interest-rate expectations.”