![[uns] house of commons, parliament](https://ifamagazine.com/wp-content/uploads/2024/11/tommao-wang-gdbj1IFvD6U-unsplash.webp)

Despite efforts to restore credibility, the UK’s fiscal framework is struggling to convince markets. With growth slowing, inflation sticky and political risks rising, investors may be looking for realism over rigidity

Daniel Casali, Chief Investment Strategist at Evelyn Partners, the UK wealth manager, comments:

Chancellor Rachel Reeves revised the UK’s fiscal rules in the last budget in October 2024, aiming to bolster the government’s credibility with investors and reduce its borrowing costs. The new rules require the government to balance the day-to-day budget (excludes public investment) by the end of this parliament and target a reduction in the public sector net financial liabilities ratio. These measures were largely intended to reassure investors that the UK is committed to fiscal discipline.

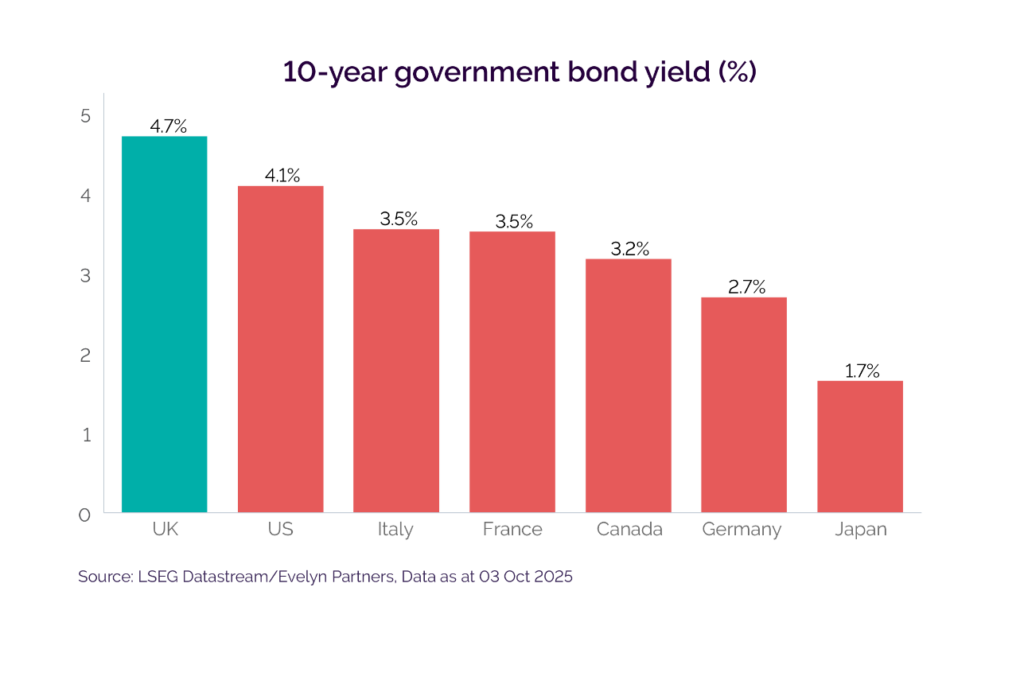

These changes have yet to deliver the intended results. The UK now holds the unwanted distinction of having the highest 10-year government bond yields among developed economies. At the time of writing, the 10-year gilt yield stands at 4.7% – higher than both Italy and Greece, despite those countries having much higher public debt-to-GDP ratios.

Nevertheless, gilt yields are not solely a reflection of fiscal policy. They also capture expectations around short-term interest rates, inflation and broader monetary conditions. A similar dynamic is playing out in the US, where investors are increasingly focused on fiscal sustainability, particularly given widening budget deficits. In both cases, markets are sending a clear signal: fiscal credibility matters, but so do inflation and interest rate expectations.

In short, several factors are contributing to the increasing cost of UK government borrowing relative to other G7 Nations:

- The UK appears to be trapped in a stagflationary environment, where sluggish growth creates doubts over fiscal sustainability.

- The UK is forecast by the OECD to post the highest inflation rate among G7 nations this year. The Bank of England’s relatively tight stance and persistent inflation pressures have contributed to elevated yields.

- Signs of public dissatisfaction with the government, as evidenced in opinion polls, raise concerns about political stability—an important consideration for gilt investors.

Ultimately, the UK government’s credibility in the bond market is earned through realism, not just fiscal discipline. As such, asset allocators will probably be focused on three main issues in the run-up to and after the Budget on November 26.

1. The growth outlook

The Office for Budget Responsibility (OBR), the UK’s fiscal watchdog, is widely expected to downgrade medium-term growth forecasts. In the OBR’s Spring 2025 commentary, it highlighted that their productivity projections have been revised downward.

Slower growth has immediate fiscal consequences. JP Morgan estimates that if real GDP growth is downgraded by just 0.1–0.2%, it would create a budget shortfall of between £9–£18 billion. In essence, the UK could be falling into a self-perpetuating cycle – as taxes are raised to fill fiscal gaps, the likelihood of recession and further revenue shortfalls increases. This makes the task of fiscal consolidation even more challenging.

2. Fiscal headroom

The government would need to find £50bn in savings to achieve a modest £10bn of fiscal headroom by 2029, according to an August estimation from the National Institute of Economic and Social Research, a politically neutral think tank. This is a challenge considering most government spending commitments were locked in during the summer spending review.

Efforts to find further savings are complicated by internal Labour Party divisions, with MPs rebelling against measures such as means-testing the Winter Fuel Allowance and cutting welfare spending.

This leaves tax increases as the primary lever to balance the books. However, the Labour manifesto pledged not to raise any of the “big three” taxes – National Insurance, VAT, or income tax – which together account for nearly 75% of total tax revenues.

There will be scrutiny on how the Chancellor can credibly raise additional revenue. Potential options could include closing tax loopholes, reforming capital gains and inheritance tax. However, each option comes with political and economic trade-offs.

3. Political stability

The Labour Government’s popularity has fallen to new lows in recent opinion polls. If current opinion polls trends continue, Reform UK could win 301 seats, according to Electoral Calculus, a UK based specialist in election forecasting. That’s below the 326-threshold for a majority in the House of Commons. Labour would drop to 153 seats (down from 412 in 2024), and the Conservatives to just 51 (down from 121).

There are multiple reasons for the decline in Labour’s popularity. Policies, such as restricting Winter Fuel Allowance eligibility and cutting welfare, which subsequently forced U-turns, have not been well received by the public.

The issue of immigration is also an important factor to the electorate. According to pollster YouGov, the public nationally believes that the most important issue facing the country is immigration and asylum, slightly ahead of the economy. Managing immigration has proven difficult for the government: the recent “one in, one out” policy agreed with France on illegal immigration comes with legal challenges and is yet to show clear signs of effectiveness.

Given these polling trends, gilt investors will be watching closely to see if the Budget can revive Labour’s popularity. If not, there is a risk of leadership challenges and internal party strife – developments that would further undermine confidence in the UK bond market. Andy Burnham, for instance, the Mayor of Greater Manchester, has hinted at a possible challenge for Kier Starmer’s job. His economic stance of criticising the UK’s dependence on financial markets and proposing £40bn in borrowing for housing is a concern for investors, where such moves could unsettle bond markets and drive-up gilt yields.

Three potential scenarios we could see in November

The Chancellor faces a complex challenge to drive-up economic growth, balance the books and manage the inevitable political headwinds, while maintaining confidence among gilt investors. With this in mind, here are three potential outcomes from the Budget and what it could mean for UK financial assets. Our focus is mainly on gilts, as these are usually more sensitive to fiscal policies.

Scenario No. 1: Muddle through.

Arguably the most probable outcome, in this scenario the Government implements modest tax increases while adopting a ’wait and see’ approach. It assumes that the OBR does not materially revise down its growth estimates.

The Government could opt for a few manifesto-compliant tweaks, preserving around £10bn of fiscal headroom. This approach may result in higher taxes for wealthier households, some of whom may choose to leave the UK.

If the government targets high-income earners or wealth taxation, it risks missing revenue expectations. Even if successful, the limited fiscal headroom may fail to reassure gilt investors.

Implication for gilts: Short-dated gilts may find support from more accommodative monetary policy. However, this muddle-through strategy is probably unlikely to restore confidence in the government’s ability to manage its finances, which may largely impact long-dated gilts.

Scenario No. 2: Large-scale tax rises.

Faced with a significant fiscal shortfall, in this scenario the government acknowledges the deteriorating state of public finances and abandons its pre-election tax promises.

To restore fiscal credibility, broad-based tax increases, including on some working households, are introduced within the next year, aiming to close the gap and create at least £20bn in fiscal headroom, even if it comes with weaker growth.

While these tax hikes may stabilise the fiscal outlook, they could undermine business and consumer confidence, especially given the UK’s already fragile private sector demand. Some measures, such as a VAT increase, could be directly inflationary, while others, like corporate tax hikes, might indirectly raise prices if businesses pass costs onto consumers.

Implication for gilts: Lower growth could reduce tax revenues and lead to a higher social security bill, creating another fiscal black hole for the government to fix. This would likely raise concerns about fiscal sustainability, which may put upward pressure on longer-maturity gilt yields over time.

Scenario No. 3: Relax the fiscal rules along with spending cuts.

This does not look likely, especially given the Chancellor’s reluctance to alter the fiscal rules so soon after introducing them and the unwillingness among Labour to agree to spending cuts. However, with the Labour Party languishing in opinion polls and the unemployment rate creeping up, albeit from a low level, political pressure to ease fiscal discipline is mounting.

Two-thirds of Labour MPs oppose the Chancellor’s fiscal rules, according to a June survey by Survation, a UK-based market research and public opinion polling company. She may consider modifying the rules while introducing wealth taxes to appease the party’s left wing and attempt to reassure gilt investors.

Implication for gilts: Ironically, this could end up being the most positive outcome for long- and short-dated gilts beyond the short term. It would remove the fiscal straitjacket to provide greater flexibility to support growth and tax revenue generation. A more flexible, transparent framework could enhance fiscal credibility through realism. This could also force the Bank of England to stabilise the gilt market, similar to the ‘mini-Budget’ under the Conservatives in Autumn 2022.

To summarise, the UK’s fiscal rules were designed to restore market confidence, but in a fragile economic and political environment they risk doing the opposite. With growth slowing, inflation elevated and political uncertainty rising, investors may increasingly favour realism over rigidity.

Whether through a strategic recalibration by Chancellor Reeves or a future shift under a Reform UK government, a more flexible fiscal framework could ultimately prove more supportive for gilt returns in the long run.