Advisers need to ensure their research into EIS is robust but are being held back by a lack of information, says Keith Hiscox, Chief Executive of Hardman & Co.

EIS has gone from strength to strength in funding growth companies and has had a material impact on employment. Unfortunately, the analysis and research of this asset class has not matured in step and remains inadequate for advisers and investors.

Many are kidding themselves if they think that ‘research’, which is little more than ‘cut and paste’ from a manager’s website or advertorial copy, is going to be deemed adequate. This research gap is holding EIS back from being considered a mainstream asset class.

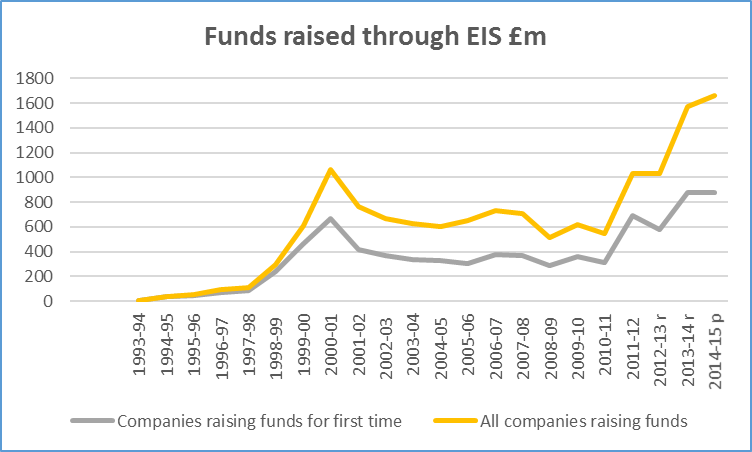

Let’s not be shy here. EIS has been a great success in funding growth companies and creating jobs. Since inception in 1993/94 £14 billion has been raised, and recent years have seen an acceleration. The latest data from the HMRC demonstrates this:

Source: HMRC, Hardman & Co

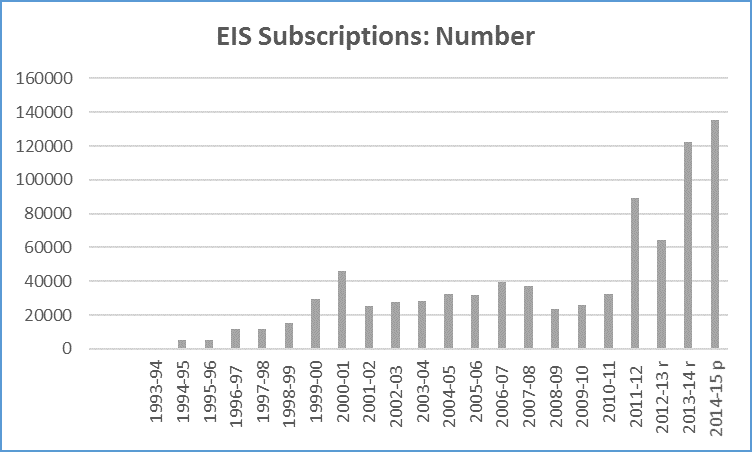

EIS has also been a big hit with investors. Recent years have seen a sharp uptick in the number of subscriptions with more than 135,000 being made in 2014/15, the latest tax year for which HMRC has published. Clearly, increasing restrictions on high income earners making provision for their pension is one of the drivers, as is the growing evidence that EIS can deliver very satisfactory returns. These suggest a bright future for advisers that understand the field well.

Source: HMRC, Hardman & Co

But the EIS world has an image problem. It is seen as risky and overly focused on tax benefits. Many commentators are, in particular, concerned about the poor quality of research in this investment class. Even the Financial Conduct Authority has fired a warning shot. In a paper published in February, the regulatory body found that many advisory firms ‘demonstrated inconsistent and insufficient research’ and that the poor quality of research and due diligence across many investment products is a root cause of sub-standard results for consumers.

Too often advisers and investors focus on the tax benefits and not the underlying investment. They plunge into EIS companies and schemes without understanding the investment they are making. Not surprisingly they can unwittingly get caught in risky ventures and the EIS world gets a bad name.

The mindset of the EIS world can perhaps be gauged by the language used. Many participants talk of ‘tax-efficient’ investing; in fact, one ‘research’ house even includes that phrase in its name. Another party uses the term ‘tax shelter’ as part of its report title. Both terms imply that the key (and perhaps only) driver to making an investment in an EIS product should be driving down an individual’s tax charge, rather than understanding the investment case. Hardman & Co deliberately uses the phrase ‘tax-enhanced’ – we believe that the tax benefits from EIS investing should be an extra return on the investment, not the main reason to make it. Another acceptable term is ‘tax advantaged’, which the HMRC and some participants use.

The industry’s encouragement to advisers and investors to have a mindset focused on saving tax is demonstrated by evidence from Google. A search for the term ‘EIS+Tax Relief’ returns 115,000 results, compared with 5,070 for ‘EIS+Opportunity’ and a mere 2,740 for ‘EIS+Growth’.

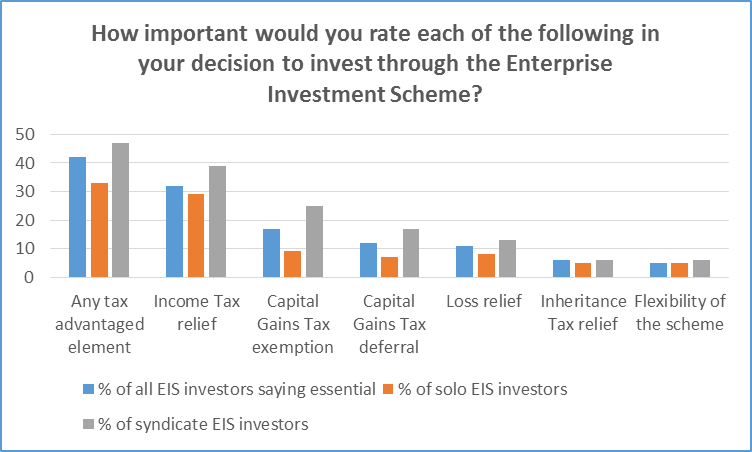

Source: HMRC, Ipsos MORI, Hardman & Co

HMRC recently commissioned a report looking at which tax benefits were important to EIS investors. The table is above. To be fair, the survey sought to explore attitudes to tax, so there wasn’t an option for investment that respondents could tick. However, qualitative interviews which followed up the survey showed that some investors, at least, had considerations other than tax:

- For some investors ‘loss aversion was a particularly important factor in decision making’

- Some investments would have been made without the tax relief because they were driven by entrepreneurial (e.g. a former businessman wanting to help start-ups in his old industry) or philanthropic reasons

- Some felt that being part of a group of EIS investors gave comfort about the business potential

There is research available on EIS to advisers and investors. Unfortunately, it often falls short of what would be considered acceptable in other asset classes. For example, much research fails to consider:

- The past performance of a management team

- Performance attribution – i.e. did one lucky investment make up for 19 disastrous ones?

- Risk analysis. The FCA paper comments that firms ‘should not rely on the provider’s opinion, for example, on the investment’s risk level’ – cut and paste won’t do

- The real fee structure, which can include hidden charges, such as a member of the manager’s team receiving payment from an investee company as a director

- The qualities of the underlying investments – not surprising since much of the work is not conducted by investment analysts, but by writers with an accounting background

In fact, much of what is loosely called ‘research’ in the EIS space does nothing more than combine factual ‘cut and paste’ from the manager’s or company’s website with the manager’s response to the research house’s questionnaire. This is not research – it is advertorial copy. It might save the advisor or investor the bother of reading the manager’s investment memorandum, but it doesn’t add value and should not be considered research by professional investors.

Some research providers have attempted to produce a scoring system. The aim is commendable – to provide a simple measure for advisers and investors. Unfortunately, the scores are entirely subjective, opaque and unverifiable. The assessment is divided into sections such as ‘Objectives/Business Model’, ‘Management Team’ and ‘Deal Flow/Exit’; a score is given for each section and a total calculated. But there are two glaring issues here.

First, there is no publicly available explanation as to how the score is determined in each section – what justifies 17/20 for one fund in one section v 18/20 for another fund?

Second, how is the weighting for each category determined? For example, one provider’s report weights the ‘Track Record’ at 40% of the score, whilst ‘Management Team/Deal Flow/Exit’ all together only merit 20%.

We are not suggesting these sector scores and weights are wrong, our point is that, without disclosure of the underlying template for scoring and weighting, the outsider can only assume that the numbers are plucked out of thin air. The idea of scoring may be laudable, but the execution is specious. Thus advisers are kidding themselves if they think they have carried out due diligence by considering these scores – if prompted by the FCA how would they explain how they are derived?

Some advisers seek to overcome the lack of analysis by advising clients to diversify – don’t put all your eggs in one individual company or fund. Such diversification should certainly be part of an investment strategy, but it should not be a substitute for research on each fund or company – how can you be sure that diversification does not mean you end up with ten duds instead of one?

In response to this need for rigorous analysis Hardman & Co entered the EIS research market less than a year ago at the behest of a number of the participants.

Hardman is an FCA registered firm, which already has a long roster of EIS clients. Our aim is to bring the analytical rigour for which we are known in other asset classes to the tax-enhanced world. The firm has a 20-year track record of writing independent research on quoted companies, with market capitalisations ranging from the smallest to £750 million.

It also carries out due diligence for investment banks, corporate finance boutiques, and private equity houses. It is asked to conduct investment case evaluations for major global businesses, family offices, sovereign wealth funds and act as expert witness in complex court cases where the valuation of a business is critical.

We have a team of investment analysts, most with more than 20 years’ experience of understanding the fundamentals of their industries and businesses and discerning the investment case and risks. Indeed, our media analyst, Derek Terrington, was cited by the Financial Times in its 2006 article ‘A catalogue of great analyst notes of our time’ for his so-called ‘crap circular’ regarding the float of the Robert Maxwells’ Mirror Group empire where his advice was ‘Cannot Recommend A Purchase’.

As the demand for EIS grows, there has never been a more critical time for EIS advisers and investors to raise their game in research and understanding. Only by doing so can the EIS industry throw off the accusation that it is all about risk, tax benefit and poor return.