Ahead of the government’s budget announcement (6 March 2024), Fidelity International urges that any future policy change has the needs of savers and investors at its very core.

With significant assets and operations in the UK, Fidelity supports clients throughout their savings journey. Whether to meet customers’ needs through their workplace pension, investment platform, direct investment or though institutional channels, Fidelity’s ambition is consistent – to support clients in achieving better financial futures.

James Carter, Head of Platform Policy, Fidelity International outlines why pension reform, ISA simplification and lower taxation for investment are paramount in fostering an environment which promotes a culture of investing and long-term saving:

- Pension Reform: Pot for life risks undermining the achievements of auto-enrolment

“We welcome the government actively engaging on the topic of pensions and its efforts to create more secure financial futures for the population. However, we worry that the proposed solution of a ‘pot for life’ intends to address issues that existing in flight policy has not yet had a chance to resolve.

“At the Autumn Statement the government put out a call for evidence on the proposed introduction of a ‘Lifetime provider’ model for workplace pensions. This is the idea that employees have the right to elect the pension scheme into which their workplace pension contributions are paid. That would be a change from the current model where eligible employees are enrolled into a scheme of their employer’s choosing.

“We believe that the lifetime provider – or ‘pot for life’ – model would radically change the UK pensions market, and we have significant concerns on the proposals being put forward. We question whether it would enable better member outcomes for typical members or deliver the policy ambitions put forward in the call for evidence.”

Fidelity recently polled1 employees on their attitudes towards workplace pensions. In principle, employees are attracted to the concept of freedom and flexibility that a ‘pot for life’ provides. Four-fifths (80%) of respondents said they should have the opportunity to choose which pension scheme their workplace pension contributions are paid into.

In reality, however, the picture is very different with a majority of employees taking comfort in the safety net their existing employer model provides. Key findings from Fidelity’s research includes:

- 65% agree that they like the idea of giving savers the opportunity to choose, but would most likely remain with the pension provided by their employer

- 50% agree that they would feel concerned about knowing the responsibility for choosing their workplace pension rests with them

- 75% agree that they like the idea of being able to choose their workplace pension provider, but would want access to advice/guidance of some kind to help inform their decision

- 51% agree that they worry it could widen the pension gap between those who are financially confident and those who aren’t

James Carter continues: “More worryingly, the proposals have the potential to undermine the role of the employer in supporting engagement in pensions and the achievements of automatic enrolment. Since its introduction automatic enrolment has revolutionised workplace saving and ensured that over 10 million2 people who were not saving for later life are now in a pension. ‘Pot for life’ proposals could be harmful to those whom automatic enrolment was designed to benefit. We need to stay focused on the successful delivery of other initiatives, such as the development of pensions dashboards, already in flight, and turn soonest attention to increasing the levels of pension contributions being made.

- ISA Simplification: helping savers to become investors

“Most people will find themselves managing a series of evolving financial objectives over time. However, we know that many find it difficult to identify which products best suit their saving needs. This complexity destroys confidence, leaving many individuals missing out on vital opportunities to strengthen both their short and long-term financial position. Further proliferation of ISA types can create confusion for investors, but also can limit the economies of scale that providers can offer. This can stifle innovation and worse, can raise costs for end investors. Simplification and certainty of tax treatment can allow both savers and companies to better plan and manage the products.

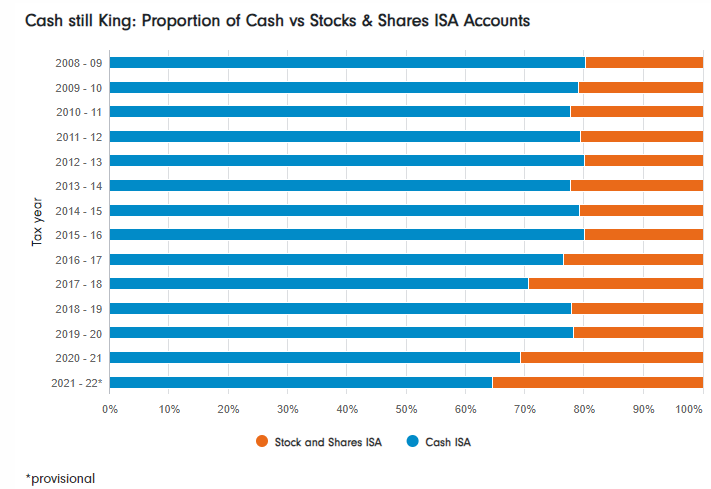

“There is an opportunity to simplify and shift a cash savings culture into long-term investing. This could be achieved by combining Stocks and Shares and Cash ISA products as well as improving the ease of transfers. Short term needs are well served, but it leads to consumers holding large cash balances for too long, missing out on higher investment returns. Cash ISAs predominate – as shown in the chart below.

Source: HMRC, June 2003

Great British ISA

“Recent reports suggest a ‘Great British ISA’ is once again on the cards, allowing savers an additional £5,000 to their ISA allowance with money directly invested in UK listed companies only. We believe it would be challenging to deliver and it’s not as clear cut that UK listed companies would automatically provide more UK investment.

- Lower taxation on investment: supporting UK Plc

“As discussions on the attractiveness and competitiveness of the equity market in the UK continue, we wanted to highlight two areas where we see potential to support improved demand, liquidity, potential returns for investors and support companies considering listing in the UK.

Stamp Duty for equity transactions – “We support the Government removing the burden of stamp duty in the UK which significantly increases transaction costs, reducing velocity of trading and allocation of risk capital by equity market participants, thereby hampering liquidity, raising the equity risk premium and fundamentally impairing valuations of UK listed equities compared to other markets where such a transaction cost does not exist.

Dividend Tax Credits – “Changes to the tax recoverability on dividends in 1991 and the abolition of advanced corporation tax dividend tax credits in 1997 have reduced the attractiveness for pensions of investing in UK equities – demand has been further impacted by the constant tinkering with allowances, reliefs and tax rates. Investing in listed and unlisted UK could be made more attractive to a wider number of people through tax incentives, such as simplifying capital gains tax and / or reintroducing indexation to encourage longer term investing. We would encourage consideration of a lower tax rate for UK dividends.”

![[UNS] tax](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/788955-featured-300x200.webp)

![[uns] house of commons, parliament](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/788873-featured-300x200.webp)