4. The US Senate remains Democrat

It seems almost a no-brainer to suggest that the US Congress will be Republican after the mid-term elections on 8 November 2022. President Biden is the least popular post-WW2 president (except Donald Trump) at this stage of the presidency and that is usually a good barometer of the swing away from the party of the incumbent president (see analyses done by FiveThirtyEight, for example, which shows that his net approval rating has slipped from +17 upon entering the White House to -8.4 now). The Republican Party also has a slight lead in generic ballot polls (asking which party an individual intends to vote for). However, the Senate elections are hard to predict with only 34 of the 100 seats up for grabs (20 of which are currently Republican and 14 Democrat, with five of the Republicans retiring versus only one Democrat). The eight seats that are not considered relatively safe for the incumbent party (Arizona and Georgia, for example), are currently split equally between the two parties. With the Republicans only needing a single net gain to take control, the odds may be stacked in their favour. But with all the uncertainties, we suspect a surprise is possible. A Republican House and Democrat Senate would still make life difficult for President Biden but not as much as if the Republican’s made a clean sweep (it could also carry a message for the Trump presidential campaign).

5. Australia changes government and emissions policies

Prime-Minister Scott Morrison’s Conservative government has now set a net-zero target of 2050 but our analysis suggests that, on recent trends, net-zero CO2 emissions will not be achieved until 2080 (see Economic Transition Monitor). Indeed, Australia has faced a lot of criticism from the rest of the world for its refusal to fully engage with the climate change issue. As a large producer of coal it has a vested interest in delaying mitigation actions (The BP Statistical Review of World Energy suggests that in 2020 Australia accounted for 14% of the world’s coal reserves and 6% of its production). However, opinion polls suggest there will be a change to a Labor government at the next election (to be held on or before 21 May 2022). The Labor Party of Anthony Albanese has committed to a 43% cut in emissions by 2030 (compared to 2005 levels) versus the 26%-28% cut committed to by the government of Tony Abbott in 2015 and the 35% forecast (but not commitment) of the current government. A change of approach and attitude could bring Australia back into the developed world mainstream on this issue, though it will be interesting to see how it impacts the export of coal to China (and indeed overall relations with China).

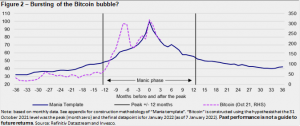

6. Bitcoin falls below $30,000 during 2022

Last year we spoke of Bitcoin falling below $10,000 but instead it reached a peak of around $68,000. The mass marketing of Bitcoin reminds us of the activity of stockbrokers in the run up to the 1929 crash (as brilliantly described in John Kenneth Galbraith’s The Great Crash, 1929). We know how that ended and Bitcoin has already fallen to around $42,000 (as of 7 January 2022), following closely the downward path of our mania template (see Figure 2). That template suggests a loss of 45% is experienced in the 12 months after the peak of a typical financial mania. If that pattern is followed (assuming we have seen the peak), the price of Bitcoin would fall to $34,000-$37,000 by the end of October, depending upon whether we use daily or monthly data to define the peak (the latter is used in Figure 2). The template also suggests that bubbles typically deflate for a further two years. Hence, we think it is not too much of a stretch to imagine Bitcoin falling below $30,000 this year (with the health warning that we have got this wrong before and that it seems to be going through a series of bubbles).

7. Turkey government debt outperforms

As we noted in the recent 2021 in review, Turkey’s currency and financial market performance has been hampered by misguided policy decisions. The country appears to be caught in an inflation/currency depreciation spiral (the lira declined by 44% versus the USD in 2022 and CPI inflation reached 36% in December). This could make it un-investible but there is a price for everything and sometimes the best opportunities appear in the darkest of moments. The yield on 10-year USD denominated Turkish Government bonds is currently 8.0% (as of 7 January), while the 5-year yield is 7.8% (compared to 1.5% for the US, 3.3% for Brazil and 2.8% for Russia). That is quite a cushion, unless of course Turkey defaults.

![[UNS] tax](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/788955-featured-300x200.webp)

![[uns] house of commons, parliament](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/788873-featured-300x200.webp)