As tomorrow is Earth Day, Michael Rae, fund manager at M&G Investments, has commented on the investment opportunities. He also highlights the importance of being selective as the dispersion between the winners and losers in the energy transition is significant.

He says:

If we rewind thirty years, 60% of the electricity consumed by a UK home was derived from coal, 10% was from oil with the balance from nuclear and hydro. Today, renewables and natural gas are roughly equal at 40%, while coal has declined close to zero, only being used in times of extreme shortage. The energy transition is well underway. The UK has among the most ambitious decarbonisation targets in the world for power, targeting Net Zero emissions from power generation by 2035. Actions over the next few years will determine whether such goals are achievable, whether power generation and the grid can be modernised in time, and what consumer acceptance of EVs and heat pumps is really like.

As we look around the world for climate solutions providers we are, more often than not, impressed and surprised at the level of innovation and creativity which is being applied to bringing about a decarbonised and circular economy. Entirely new industries and value chains are being created in front of our eyes, with much of the new thinking coming from comparatively small and nimble enterprises. That said, we spend as much time thinking about business model quality as we do about the positive impact, as we term it, that the companies we are invested in are having.

Our experience has been that a rising tide does not lift all boats. Entirely new industries and value chains are being created in the shift to decarbonise and although the energy transition creates a durable growth runway for many companies, which will ultimately drive share prices, dispersion between the winners and losers is wide. Taking the global solar sector alone, the spread between the best and worst performing equities on our watch-list over the past year has been greater than 100% (+85% for the best vs -45% for the worst). Simply being exposed to a growing end-market is not enough. This is why we favour a diversified portfolio of companies with varying end-market characteristics, with each investment made based on the quality of the business model, as well as the durability of the underlying market dynamics.

Here are examples of businesses that are in the driving seat, benefitting from government policy and/or consumer behaviour change:

Alfen: EV-charging & energy storage

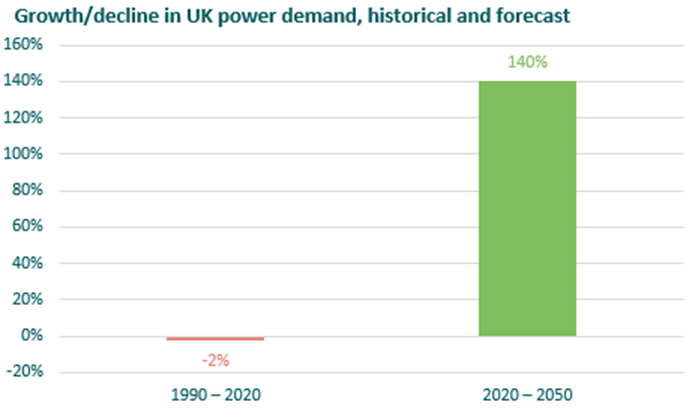

Forecasts from the UK Climate Change Committee expect more than a doubling in electricity demand over the next 30 years, largely due to increasing use of electric vehicles and heat pumps. This stands in stark contrast to the past 30 years, in which UK power demand has been stable, and indeed has slightly fallen. These shifting patterns of consumer behaviour have profound implications for everything from the generation of power, its transmission via high-voltage direct current (HVDC) around the country, and the way we interact with it in the home, in the form of EV-charge-points and behind-the-meter storage.

One beneficiary of these trends in the UK, and similar dynamics in Europe, is likely to be Dutch company Alfen. With close to a century of experience in building grid equipment, Alfen is present across the power value chain, providing transformer substations, utility-scale batteries and EV-charge-points for use in the home or at destinations such as shopping centre car parks. Alfen is a rare, possibly unique, example of a company operating in these new markets which already demonstrates profitability. Most like-sized competitors are pre-profit and reliant on growth prospects to support their valuation. We expect policy developments in the EU and UK combined with company-level Net Zero targets to continue to support demand for Alfen’s products.

Tomra: Plastic recycling

The prospect of ending plastic use remains a distant one, and as a material plastic remains unrivalled in terms of cost, weight, and versatility of use. The good news is thanks to continued innovation, more and more plastic types are now recyclable through chemical processes, allowing the original fossil molecules to be re-used. However at this stage, globally only 9% of plastic waste is recycled while 22% is mismanaged. In pursuing the Reduce, Reuse, Recycle approach, all participants, from the petrochemical companies, to the packaging compounders, to those selling consumer goods, and the end consumer itself are having to play a part.

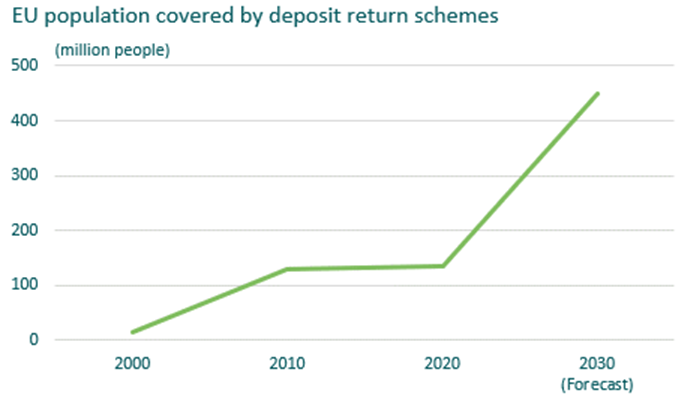

Nowhere is this more clear than in the EU, which, already a leader in plastic circularity, is again stepping up the pressure for change via policy. In November 2022, the European Commission proposed that all EU member states should implement a Deposit Return Scheme (DRS) for metal and plastic beverage containers by 1 January 2029, expanding on schemes already implemented in the likes of Germany, Denmark and Sweden. A UK scheme is also currently proposed covering England, Wales and Northern Ireland, from 2025, and separately for Scotland, possibly as early as August 2023 (**Note: The new First Minister in Scotland Humza Yousaf is considering pausing the scheme**). Studies show container collection rates in countries with DRS consistently rise to 90%. The economics are also quite neat, with the unclaimed deposits from the unreturned containers contributing to, or even covering, the costs of the wider scheme.

To us, the stand-out beneficiary is Norwegian company Tomra, which is the global leader in manufacturing both reverse-vending machines, for collecting recyclable waste, and waste sorting machines, which are installed at recycling centres. Tomra has a rich history of innovating in this niche field, and indeed the company’s founders invented the world’s first automated reverse-vending machine in the early 1970s. Tomra’s business goes right to the heart of the issue with waste sorting as, even if all materials have ended up in the right bin, they still need to be sorted by plastic type, colour, and to assess the presence of labels and lids, before they can enter the chemical recycling process. Sophisticated scanning technology like that of Tomra is taking an increasing amount of the burden off the consumer, raising the likelihood of adoption of DRS. In 2022, the avoided carbon emissions enabled from Tomra products in use by customers was just over 21.1 million tonnes of CO2 equivalents, representing an 8.7% increase from 2021. The total avoided emissions compare to about 35% of Norway’s greenhouse gas emissions in 2021. Tomra machines collected more than 45 billion containers in 2022.

Ceres Power: Decarbonising the internet

We now expect access to our data and to the internet to be continuous and uninterrupted. This creates a headache for the operators of data centres, the large hubs which store and process the flow of data from the apps and devices we use every day. Data centres are enormously power hungry, and their reliability is tied to the quality of the underlying power grid. The share of digital technologies in global greenhouse gas emissions has increased by half since 2013, from 2.5% to 3.7%. If there is a power cut because of extreme heat, extreme cold, or even just a tree falling down in the wrong place, the instability of the grid feeds leads directly to disrupted data relaying and storage. For this reason, today’s data centres are built with several layers of diesel generator sets, designed to kick in during periods of grid instability. Although used infrequently, these diesel-powered machines are not compatible with the Net Zero emissions commitments which are widespread in the technology space.

One solution is hydrogen-powered fuel cells, which operate in the same way as diesel-generators, providing fast-response, consistent power, but are fuelled by an on-site store of hydrogen, which itself can be produced cleanly via renewable power. The UK is home to one of the leading providers of technology in this area, Ceres Power. Ceres differs from most companies operating in the hydrogen space, because it doesn’t want to be a manufacturer, it simply wants to license its fuel cell design, the ‘SteelCell’, to large-scale global manufacturing companies who already have a global sales and distribution network.

This approach removes the need for expensive factories, which bring high costs and operational risk, and makes for very high gross margins, since Ceres is capitalising on the repeated sale of the same design. In our view, this means Ceres is closer to sustaining itself from its own cash flows than can be said of its peers. Customer endorsement is also very encouraging – Ceres is working closely with Bosch, one of the world’s largest appliance and industrial technology companies, based in Germany as well as Doosan and Weichai in Asia.

![[uns] house of commons, parliament](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/788873-featured-300x200.webp)

![[UNS] tax](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/788955-featured-300x200.webp)