Despite slowing growth and conflicting forecasts, fund managers remain cautiously optimistic on stock market returns, Quilter’s Investor Trends Survey shows. Investors expect Jerome Powell to stay as Fed chair, though inflation and limited rate cuts keep risks in play.

Despite a strong rally in investment markets following ‘Liberation Day’ back in April and weakening economic growth indicators, fund managers remain optimistic about market returns going forward according to Quilter’s latest Investor Trends Survey.

Asked to rank their current risk appetite on a scale of one (very bearish) to 10 (very bullish) on a six-to-nine-month basis, the average score was 5.4, suggesting fund managers do not want to take risk off the table at this stage.

Markets have performed strongly since Donald Trump first announced the introduction of punitive tariffs on 2nd April, with the MSCI USA index rising by 24.5% since it hit its trough soon after, and up 2.2% since the start of the year.*

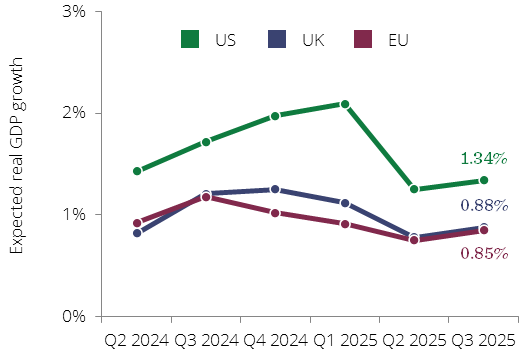

It also indicates we are in somewhat of a contrarian market as expectations remain weak for real GDP growth. At the beginning of the year, investors expected real GDP growth in the US for 2025 to be over 2%. However, fast forward to now and those expectations are at just 1.3% for this year and at 1.6% for 2026. While the recession risk in the US has receded, growth is proving harder to come by for the world’s leading economy.

The UK and Europe have similarly weak prospects, although the downgrade has not been as severe. 2025’s expectations sat just over 1% for the two regions at the beginning of the year but have fallen to 0.88% for the UK and 0.85% for Europe respectively.

What are your expectations for real GDP growth in 2025?

Source: Quilter’s Investor Trends Survey

With such soft GDP growth, you would expect this to be the precursor for interest rate cuts. However, on average, respondents think US interest rates will finish 2025 at around 4% and will only drop to 3% by the end of next year. Usually in a low growth environment we might expect more significant rate cuts, but with inflation expected to be around 3% by the end of 2025 (up from 2.45% when asked the same question a year ago), this could tie the hands of the central bank.

Furthermore, respondents do not anticipate inflation to come down at all, expecting it to come in at 2.8% at the end of 2026. If this plays out then investors are expecting a small drop in inflation from 3.0% at the end of 2025 to 2.8% 12 months later. This would appear unlikely to be enough to allow for a whole percentage point cut in rates, unless unemployment rises sharply.

Finally, while the path for interest rates in the US looks uncertain, investors do not expect Donald Trump to act rashly and fire current Federal Reserve Chair Jerome Powell, as has been rumoured of late. While Donald Trump is desperate for interest rates to be cut, just 12% of our respondents think Powell could be ousted before his term officially ends in May 2026.

The survey, which was sent to 21 of the leading fund management institutions representing £22 trillion of assets, is carried out on a quarterly basis and covers forecasts for macroeconomic data and timely indicators.

Lindsay James, investment strategist at Quilter, commented:

“News of slowing GDP growth, sticky inflation, tariffs, and interest rates getting stuck would suggest now is the time to be bearish. Indeed, after a strong rally following the ′Liberation Day’ induced falls in April, market participants would be forgiven for wanting to take a breather and remove risk from the table. However, this appears to be far from reality and in fact fund managers remain ‘cautiously bullish’ on the prospects for future market returns.

“Valuations remain toppy in some areas, so for how long such sentiment can continue remains to be seen, but if corporate earnings continue to resist the weak economic backdrop, markets may just have a little higher to go from here. A lot of this hinges on what the Fed does with interest rates and how businesses in America deal with increased costs from tariffs.

“The market expects Jerome Powell to stay as Federal Reserve Chair, and while the US economy has not quite rolled over, it is clear it is being stressed at the seams. A sustained period of rate cuts, therefore, looks unlikely, while it will probably be the US consumer that bears the brunt of the tariffs. As such, there appears to be risks lurking around every corner for investors, but confidence clearly has not been shattered. Consequently, it will be fascinating to track the sentiments of these fund groups going forward.”

*Both figures are returns in sterling as at 25th August 2025.

![[uns] house of commons, parliament](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/788873-featured-300x200.webp)

![[UNS] tax](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/788955-featured-300x200.webp)