Short-term bonds have seen their biggest hike in 11 months, but longer-term bonds continue to offer greater returns despite stagnating. Moneyfactscompare.co.uk reveals the state of play in the fixed bond market for savers.

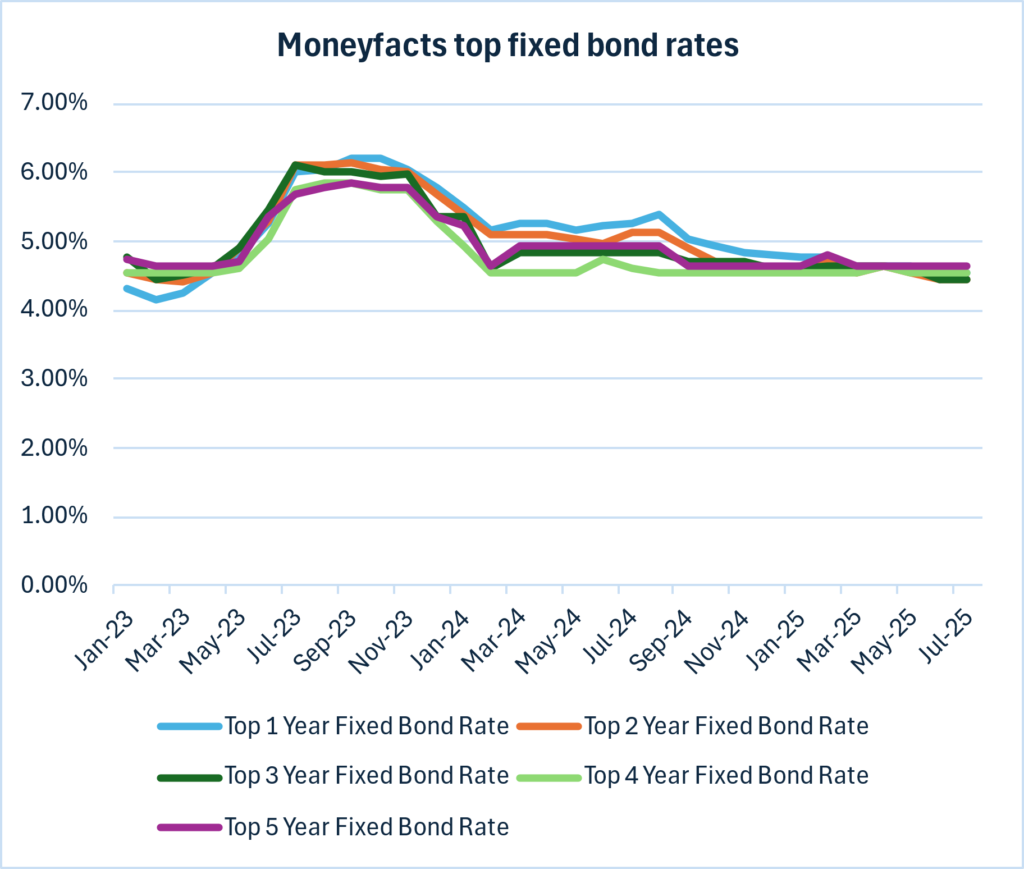

· The top one- and two-year bonds rose, with the top three-, four- and five-year bonds remaining unchanged.

· The top one-year fixed bond rose by the largest amount since August 2024 to 4.55% gross, which is 0.09% lower than the top five-year fixed bond at 4.64%. The top five-year bond rate was higher than the top one-year bond a month prior by 0.19%.

· In January 2025, the rate gap between the top one- and five-year bonds was 0.15%, as they sat at 4.79% and 4.64%, respectively.

· A year ago, the top one-year bond paid 5.25%, with the top five-year bond paying 4.95%, a gap of 0.30%.

| Savings market analysis – top fixed bond rates | |||||||

| Jan-23 | Jul-23 | Jan-24 | Jul-24 | Jan-25 | Jun-25 | Jul-25 | |

| Top one-year fixed bond rate | 4.33% | 6.02% | 5.50% | 5.25% | 4.79% | 4.45% | 4.55% |

| Top two-year fixed bond rate | 4.56% | 6.10% | 5.40% | 5.13% | 4.65% | 4.44% | 4.45% |

| Top three-year fixed bond rate | 4.76% | 6.10% | 5.35% | 4.85% | 4.61% | 4.45% | 4.45% |

| Top four-year fixed bond rate | 4.55% | 5.75% | 4.93% | 4.60% | 4.54% | 4.54% | 4.54% |

| Top five-year fixed bond rate | 4.75% | 5.70% | 5.22% | 4.95% | 4.64% | 4.64% | 4.64% |

| Top interest rates based on a £10,000 deposit as at the start of the month. | |||||||

| Source: Moneyfactscompare.co.uk | |||||||

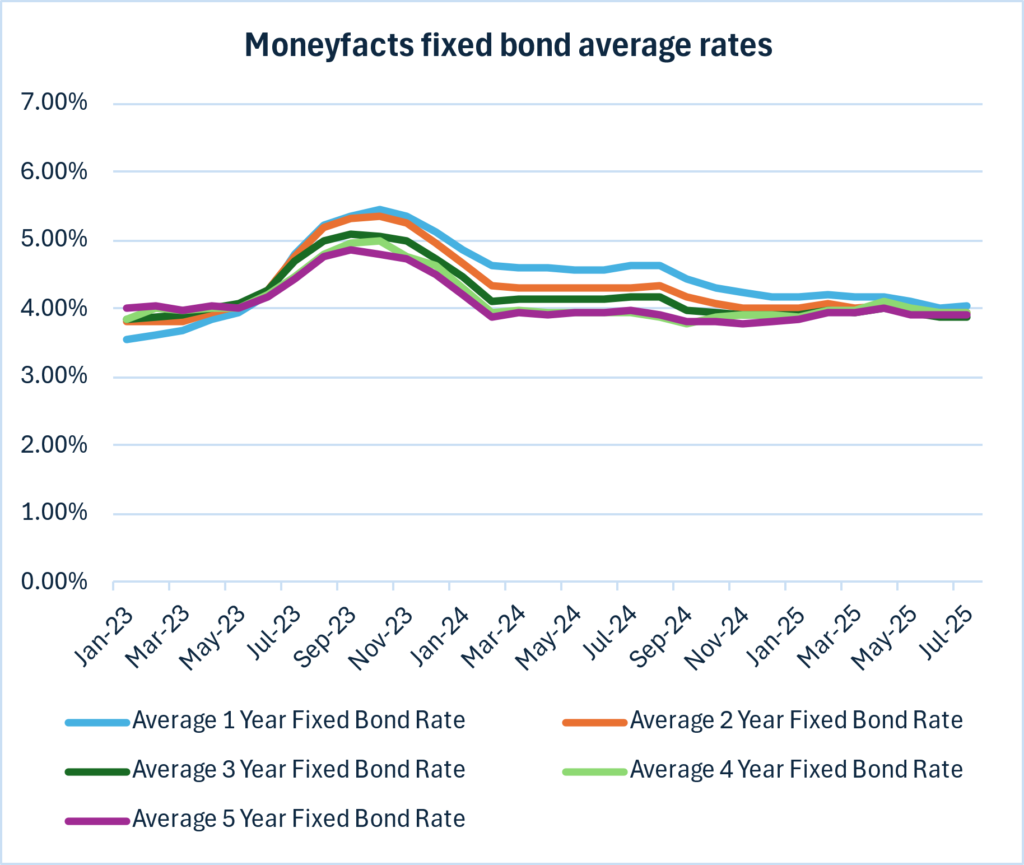

· The average one-year fixed bond rate at 4.04% gross is now 0.13% higher than the average five-year fixed bond at 3.91%. The rate gap was 0.11% a month prior.

· In January 2025, the rate gap between the average one- and five-year bonds was 0.33%, as they sat at 4.19% and 3.86%, respectively.

· A year ago, the average one-year bond paid 4.64%, while the average five-year bond paid 3.98%, a rate gap of 0.66%.

| Savings market analysis – average fixed bond rates | |||||||

| Jan-23 | Jul-23 | Jan-24 | Jul-24 | Jan-25 | Jun-25 | Jul-25 | |

| Average one-year fixed bond rate | 3.56% | 4.80% | 4.87% | 4.64% | 4.19% | 4.02% | 4.04% |

| Average two-year fixed bond rate | 3.83% | 4.77% | 4.68% | 4.32% | 4.02% | 3.94% | 3.94% |

| Average three-year fixed bond rate | 3.84% | 4.69% | 4.46% | 4.18% | 3.92% | 3.89% | 3.89% |

| Average four-year fixed bond rate | 3.85% | 4.46% | 4.31% | 3.93% | 3.89% | 3.93% | 3.94% |

| Average five-year fixed bond rate | 4.02% | 4.44% | 4.20% | 3.98% | 3.86% | 3.91% | 3.91% |

| Average interest rates based on a £10,000 deposit as at the start of the month. | |||||||

| Source: Moneyfactscompare.co.uk | |||||||

Caitlyn Eastell, Spokesperson at Moneyfactscompare.co.uk, said:

“The top one-year bond has seen its largest month-on-month increase in almost a year. Generally, this sector of the market is more competitive as they are a good way for challenger banks to test savers’ appetites and fund their future lending. Despite short-term rates improving, investors continue to be incentivised to lock away their cash for longer as they can receive greater returns. The same drive is lacking among providers to improve their rates as the top four- and five- year fixed bonds have failed to improve for the third consecutive month, but this may be attributed to uncertainty surrounding interest rates over the long-term.

Savers coming out of the market-leading bond from July 2023 will be disheartened to see that rates have dropped by almost 2%, which equates to a £347 loss if they re-invested £10,000. To add insult to injury, initially inflation would have eroded all of savers’ returns, leaving them worse off in real terms. Even two years on, after inflation, investors are left with just over 1%.

An estimated 7.08 million taxpayers are expected to be in the higher income tax bracket, with a further 1.23 million projected to be in the additional rate tax bracket during the 2025-2026 tax year. As a result, many savers – especially those with larger deposits – could be hit with an unexpected tax bill as they find that their Personal Savings Allowance (PSA) has been halved or removed entirely.”